Guest essay by Tilak Doshi – Senior Visiting Research Fellow, Middle East Institute, National University of Singapore

It would seem that the Middle East oil producers cannot get enough of bad news these days. The coronavirus pandemic and the collapse in global energy demand in the first quarter of 2020 led to oil prices plunging into the mid-teens as Saudi Arabia launched the oil price war against Russia in early March. Despite the subsequent historic OPEC+ deal in April to slash output by an unprecedented 9.7 million barrels per day (Mbd), oil prices have been stuck around $40/barrel since June. Prospects for an economic recovery for the Middle East – which already looked precarious after the steep fall in oil prices since mid-2014 as the US “shale revolution” took hold in global oil markets — now look significantly worse than that of other emerging market regions.

BP and Shell: Cutting Oil and Gas Output

In the midst of this calamity, BP made its bombshell announcement in early August of its intentions to slash its oil and gas output by 40% by 2030 from 2019 levels, by actively managing its investment portfolio in favour of low-carbon renewable energy. The leading international oil company — known for its influential annual global energy statistics reports – had come out with its latest 2020 energy outlook that suggests that oil demand may already have peaked in 2019. As if on cue, the other European oil major, Royal Dutch Shell, reported last week a similar 40% planned cut to its oil and gas exploration and development budget to “prepare for the energy transition”.

BP’s outlook presented three scenarios – “business as usual” (BAU), “rapid (transition)” towards a low-carbon renewable energy future and “net zero” carbon emissions by 2050, of which the last two postulate 2019 as marking the global oil demand peak, steeply falling from 100 Mbd to 55 Mbd and 30 Mbd by 2050 respectively. In contrast, after recovering from the impact of Covid-19, the consumption of oil in BP’s “BAU” scenario plateaus at around 100 Mbd for the next two decades, before declining to around 95 Mbd by 2050. Evidently both BP and Shell are convinced that the likely outlook for global oil demand growth is better approximated by either the “rapid transition” or “net zero” scenarios.

Despite repeated claims about the cost competitiveness of solar and wind energy, BP’s scenarios of a “rapid transition” or a “net zero” world of carbon emissions by 2050 are ultimately founded upon government subsidies for solar and wind energy and electric vehicles, carbon taxes and policy mandates such as renewable portfolio standards. Whether the developed economies will go all out for a Green Recovery – as called for by leading figures such as European Commission President Ursula von der Leyen, chairman of the World Economic Forum Klaus Schwab and Executive Director of the International Energy Agency Fatih Birol – remains to be seen in the cold light of economic recession, record budget deficits and the need to kick-start their economies from their current Covid-19-induced comatose state. One has only to appreciate Poland’s reaction to the EU’s climate goals to be somewhat sceptical.

Middle East: Under Existential Threat?

The Middle East accounts for 48% and 38% of proven global reserves of oil and gas respectively. The announcements by BP and Shell to cut their oil and gas investments by 40% by 2030 would seem to signify an existential threat to the future viability of the region’s oil and gas producers. Yet it would take a distinctly European view of the global energy future to pay credence to such an outlook.

A senior executive of U.S. oil producer ConocoPhillips said last week that he sees global demand returning to 100 Mbd and growing from there, with oil an “important part of the energy mix in any scenario” going forward. The CEO of Chevron, Mike Wirth told an audience that the global push for clean energy “doesn’t mean the end of oil and natural gas…it will be a part of the mix, just as biomass and coal are still enormous parts of the mix today”. These views are consistent with an IMF econometric analysis of the determinants of oil demand which predicts that global oil demand will peak around 2041 at about 115 Mbd.

On the high road of the climate change crusade, sign-posted by corporate brochures extolling social responsibility and environmental sustainability, BP and Shell may be the first among the big oil majors. But that is not what makes the oil world tick. When Ali Naimi, the Saudi Arabian oil minister from 1995 to 2016, was asked in 2018 whether he saw a threat to oil demand from climate change policies and the increasing use of electric vehicles, he replied that “I would like to put everyone at ease, there are no such worries”. Cynics will say that he spoke “his book”. Yet history might be his best witness.

Developing Asia: The Need for Oil (and Gas and Coal)

Developing Asian countries accounted for just over 70% of global oil demand growth in the five years to 2019. That is, out of 7.3 Mbd growth in global oil demand over the period, developing Asia consumed 5.3 Mbd. In any credible scenario where governments retain legitimacy by delivering higher standards of living for their people, the Asian developing countries’ appetite for oil (along with gas and coal) will mount for at least a few more decades to come.

It would be implausible to believe that the developing countries in Asia, Africa and Latin America will undertake costly subsidies and infrastructure investments on intermittent and low-density “renewable” technologies – in the wake of the devastating Covid-19-induced lockdowns — rather than invest in established energy system that has been developed over the past century. China, for instance, approved nearly 10GW of new coal-fired power generation capacity in the first quarter of this year, roughly equal to the capacity approved for all of 2019. In mid-June, India opened up coal mining to the private sector half a century after bringing it under state control, in a bid to boost the coronavirus-hit economy. The International Energy Agency found that “global approvals of new [coal] plants in the first quarter of 2020 (mainly in China) were at twice the rate seen in 2019”, with a long pipeline of projects under construction. Wood Mackenzie, a consulting company, estimates that there will be a net increase in global coal-fired power capacity this year, with 22 gigawatts of closures in Europe and the US more than offset by 49 gigawatts of plants opening in Asia.

If there is bad news for the Middle East oil producers, it has little to do with peak oil demand. It would be that they failed to exploit their treasure of energy reserves to help themselves while their oil sales rescue the rest of humanity in the developing countries from the ravages of energy poverty.

Consumers should be pleased with low prices for a while.

I’m liking that aspect, although the broader economic implications are not good. We pay as little as au$1 per litre now in parts of Australia, about us$2.50 per us gallon. Thats the cheapest it’s been for about 15 years.

It’s about U.S. $1.78 to $1.95/gal in the Denver area of Colorado this week (as low as AUD $0.67/L).

It was about 30% less expensive earlier in the year, but under $2.00/gallon is quite nice. With inflation, it’s near the all time lows.

We NEVER get down to those prices in Brisbane for any fuel grade other than 91 octane … who uses that ? Prices here leap instantaneously from AUS$1.09/L to AUS$1.47/L (95 octane) and will stay there for up to 3 weeks before gradually sinking down over a 2 week period to around AUS$1.09 … and then leap straight back up again.

World oil market prices don’t seem to make much of an impression on the gouging in our state but let there be a sniffle of a minor international risk event and prices will jump to around AUS$1.65/L in the blink of an eye.

Hey CRED all Mercedes-Benz ICE engines require 91 Octane minimum. Pisses me off every time I have our 300 gallon tank filled @ur momisugly $2.65/gal (current). My Toyota Tacoma doesn’t need it, but my wife’s M-B GLC 300 does. We are in SE Pennsylvania where gas taxes are among the highest in the US. Beats the high 3’s we paid some years back.

Same situation with us. My Jeep runs on regular. My wife’s Mercedes requires 91 octane. The choices at the pump are 87, 89 and 93 octane. The guy who sold us our first MB, said the 89 octane should be OK. It wasn’t. Lots of misfires and trips to the dealership for “check engine” lights.

Our old hemi-engine Jeep Commander ran noticeably better on premium. But it was never disabled by regular.

@David Middleton OT: Saw this, and thought you would be interested: Shell removal of Brent Platform Bravo.

David, w/my old ’61 V-8 Impala ages ago, it supposedly needed high octane because of the relatively high-compression, but to save money I retarded the timing until it wouldn’t knock on regular while accelerating. Obviously alot harder to do that kind of adjustment on modern vehicles. Didn’t hurt it as it ended up w/180k miles until I sold it.

As long as rich countries distort the markets for energy through ridiculous subsidies to solar and wind the large oil companies will follow the money – as they should. It is a failure in governance, not capitalism that is driving oil prices down. If it were not my money that is going to these corrupt schemes, I wouldn’t care except in that they are destroying entire landscapes in the process – and creating a huge and expensive cleanup mess for the future.

The Middle East has at least another 10 good years of selling their product, but of course there are going to be hills and valleys in the profits. Green energy will ultimately fail and fail miserably so that is not really the issue (other then all the money wasted on it). Ultimately if Middle East countries do not develop alternate economies not based on oil, they are going to hurt – but that’s still a long ways off.

When new standardized nuclear power reactors are finally designed, signed off on, and built – THEN the oil/gas starts losing it’s relevance. 24 hour a day reliable electricity means you can actually charge a fleet of cars without causing blackouts (assuming upgrades to transmission). Meanwhile cars will continue to become ever more gas efficient.

I foresee future cities being designed without public access for cars. The central city will be reached by subways. Service roads will like be underground and restricted to goods delivery and of course used by the government elites. Cars will be relegated to being parked around the central city. If this occurs, then one of the primary problems with inner city pollution is solved without any need to force cars to be all electric.

Gee with all this plunging oil demand CO2 levels must be trending south, given we have such an impact on them……oh wait. I guess we wont look at that again until the post Covid ramp up of real world transport, then we will be allowed to notice.

Oil is only one of the fossil fuels.

Oil isn’t the only fossil fuel that can provide gasoline and kerosene. Coal can be used in the Bergius process to produce gasoline (we did it in 1948 to produce gasoline that was slightly more expensive than petroleum-derived gasoline, but of higher quality), and the Fischer–Tropsch processes to make kerosene and like products. We have enough coal to produce the entire energy requirements of humanity for 400 years.

It wasn’t too long ago (within my lifetime) that “coal tar” was the source of hydrocarbons used for the vast array of industrial products for which we now use petroleum. Our expertise at manipulating hydrocarbons on an industrial scale is vastly improved since that time. We have at least another 100 years of petroleum, so that’s 500 years of comfort zone.

By that time, 2520, nuclear fusion should just be 20 years away….

If BP and Shell reduce their oil business it would be to the benefit of Middle East producers among others that would see their market share increase.

But BP and Shell are not telling the truth. They are cutting their oil and gas investments because the price of oil and gas is too low and they need to reduce capital expenditure. Since 2018 everybody has been expected the price of oil to go above $60 again, but the COVID and resulting global economic crisis has convinced oil executives the price of oil isn’t going to recover in years. The price simply doesn’t justify so much investment. It means there will be less oil produced in the future, a.k.a. Peak Oil.

The problem is that BP and Shell plan on remaining very active in the Gulf of Mexico and other basins in which they have been successful. Even if they do cut CapEx long term, it won’t be in places where it will benefit many competitors.

What you are saying is that low prices have led to a reduction in new investment which will lead to high prices as demand increases and then investment will increase.

In other words, the market

… and BP’s lurch towards ‘ruinable’ energy !

“Peak Oil” refers up the situation where there is less oil to extract than there was previously. That is something that will affect us.

Any peak because of a drop in demand will not affect us at all. That is lower case “peak oil (demand)” and nothing to worry about.

No. Peak Oil refers to less oil being extracted than it was before. Nobody knows how much oil is left and it is irrelevant to Peak Oil. Peak Oil could happen with a huge amount of oil in the ground, the same way Peak Whale Oil took place when there were still quite a lot of whales in the oceans.

Whether Peak Oil is important or not depends on where do we get the increasing amount of energy we need and at what cost. That we try to get it from the wind and the sun is not a good sign.

Zig Zag is exactly correct…

This refers to the recoverable resource, not the volume of oil in the ground (oil in place).

Peak Oil will occur when we have produced approximately half of the oil we will ever produce. The estimated ultimate recovery (EUR) is an unknowable fraction (recovery factor, RF) of the unknown original oil in place (OOIP) volume.

EUR = (OOIP x RF) x Recovery Effort

The peak production rate of a basin or play is generally achieved when half of the EUR has been achieved. Uneven advances in technology often prevent the curve from being perfectly symmetrical.

OOIP is entirely geological.

RF is a combination of reservoir mechanics technology.

Economics and politics dictate the effort made to recover the resources. The economics are driven by product prices (supply & demand) and extraction costs (a function of technology and experience). Politics determine whether or not an effort can be made.

Wikipedia has it correct:

“Peak oil is the theorized point in time when the maximum rate of extraction of petroleum is reached, after which it is expected to enter terminal decline.

…

It is often confused with oil depletion; however, whereas depletion refers to a period of falling reserves and supply, peak oil refers to the point of maximum production.”

https://en.wikipedia.org/wiki/Peak_oil

The curve of oil production doesn’t have to be symmetric. Half of oil ever produced doesn’t have to take place close to the peak in production. And geology doesn’t have to be the main reason for Peak Oil. All of those are simply assumptions. The only thing that has to take place for Peak Oil is that the rate of production decreases permanently.

I would think that both Shell and BP are just going to sell off their high cost production and concentrate on what makes them the most money. A sound business plan. Loss cost producers will pick up the assets sold by Shell and BP and make them produce more oil at a lower cost for a much longer time.

Anyone who has ever worked for either Shell or BP is well aware that they do “nothing” on the cheap.

I worked for Shell in Houston for several years out of grad school and one of my mentors there used to say, “Why buy 1 when you can buy 7.”

Hi Javier, et al,

No matter what BP and Shell are actually planning, and depsite all the feel good hot-air from the Gang-green cheer squad about investors and the market forcing eevil big oil to mend it’s ways and go green, or the pin doctors harping ad-nauseum about the great opportunities to be harvested by greening porfolios, in the real world both BP and Shell have seen real investors and real markets reward their stated green ambitions by driving both companies’ share value down to the lowest they’ve been in a quarter of a century. I guess we should be watching to see how low Total sinks next, since this forced ‘energy transition’ seems to be a primarily European mental affliction.

It is not BP and Shell green ambitions what has driven down their valuations. The entire energy sector broke down in 2014 and never came back.

We developed a problem in 2005 with the then peak in conventional oil. The increase in unconventional oil (LTO and oil sands mainly) was the answer but it didn’t fix the problem. The problem resurged in 2014 in a different form with the oil price crisis. Everything points to a future with less energy, not more. Energy companies are at the center of this energy crisis.

Blah, blah, and blah blah. When it gets down to it the world will get back to using more oil than ever when the pandemic subsides and we return to economic stability. And for all the talk about oil companies investing in renewable energy show me what they’ve really done other than a virtue signal here and there? They know they have a lock on energy for the foreseeable future. Sleeping with dogs gets you fleas.

Great post Tilak… 👍👍

Dear David — thanks for the appreciation.

And I can only echo David’s comment, Tilak!

As always from you, a thoughtful and well-considered article that highlights the realities behind the latest PR manoeuvres from BP& Shell.

Thanks for the insight & analysis!

👌👍

The historic peace deals Israel has signed with UAE and Bahrain has signaled a new outlook by the Middle East oil sheiks as shifting realities of less money to fund military forces are setting. It is an outlook that they can no longer afford to fight with Israel while maintaining their own standards of livings, whilst the real, more immediate threat seems to be an evolving Iran-Syria-Russia axis. The common enemy of a coming nuclear-armed Iran along with the fiscal reality of much reduced oil income is uniting all of them.

And the US Democrats’ promise, including Joe Biden and Kamala Harris, to shutter US domestic energy production of oil and natural gas (via bans on fracking at first, then new federal land oil and gas leasing, then eventually off-shore leasing shutdowns) will return the US to Middle-East oil dependency. That will be a a development that Putin and Xi would love to see happen, because then foreign power forays and military mischief into the Persian Gulf/Middle East would once again threaten US economic and industrial output.

It had to come as a wake-up call/shock to Iran and Russia that the September 2019 Iranian drone-missile attack on the Saudi Arabia oil processing/output facilities at the Abqaiq and Khurais facilities, an attack that took-out more than 5.7 mbd of Saudi oil output in one event, was hardly registered in the US and the West oil markets with little price swings. Iran’s attack simply created a temporary price/market share opportunity for US shale oil frackers to make some more money and cover any lost supply.

https://en.wikipedia.org/wiki/2019_Abqaiq–Khurais_attack

That lack of any lasting effect of that attack surely had to unnerve the Iranians and Russian advisors. Their military and strategic oil calculations were caught woefully underestimating the strength of US oil and gas production capabilities providing extra supply capacity to the world’s markets, and the inability to disrupt that. An entire re-calibration of strategic thinking obviously has been on-going in Iran and Russia about how the Persian Gulf oil supply disruptions can be used for strategic advantage in a showdown with US and Saudi and Israel forces. Everyone now of course waiting to see how the US Presidential election turns out before making any more moves.

Then of course it unnerved Iran mightily when President Trump took out the likely mastermind behind the Saudi oil facility attack, probably an assassination much to the approving nods of all the Sunni oil sheiks in the Persian Gulf. It was a done with a very fitting drone strike on Iranian Quds force commander, Gen Qasem Soleimani, on 3 January this year, who was quite audaciously, and openly visiting the Iraq extremists aligned with Iran with US military forces all around. (Maybe he forgot that Shi’ite Iran-loving Barack Obama was no longer President?)

It probably is no coincidence, that the sheiks, seeing a US able to act like that against a Senior Iranian leader and not worry about oil price shocks and supply disruptions, and dealing a real psychological blow to Iran, were key factors for the UAE and Bahrain peace deals with Israel.

So the world is watching the US election of either Biden or re-election of Trump. The Middle East will likely go up in flames in the coming years if Joe Biden becomes President and then makes good on his and Kamal’s promises to greatly throttle US energy independence via fracking bans and the like. Such a throttling of domestic energy production would of course re-chain the US to the Persian Gulf via oil dependence and thus open the entire Western world (not just the US) to blackmail and military adventurism by Iran and Russia there.

There certainly could not be anyone more interested in seeing Biden-Harris win than Vladimir Putin and the Death-to-USA Iranian mullahs and ayatollah.

Nice analysis Joel

Oil and Gas production is low on federal land or trending in the US more and more toward private land. If Komissar Biden wishes to stop fracking he has a few hoops to jump through

https://www.instituteforenergyresearch.org/fossil-fuels/oil-and-gas-production-on-federal-land-falls-far-below-historic-norms/

Bernard McCune

A nice summary what ought to be blatantly obvious to anyone following international politics rather than focusing entirely on the US. I would add one other thing.

While Biden is promising to focus billions in government spending on “made in America”, he and the press are ignoring that his attack on fossil fuels will not only make the US dependent on the Middle East, it will also allow China and Russia and others to steal jobs. Unencumbered by any constraints on fossil energy use, their cost of goods and services will be well below what American companies competing on the world stage can provide. Those companies will be faced with either shifting their production overseas to compete, or losing market share to those that do. Either way, the US economy will lose trillions, not billions.

Joe — excellent prognostications. One would hope though that the pragmatic pressures of office might constrain a future Biden administration from the Green lunatic fringe, but if the past few months have shown anything, it is that Biden and his entourage is increasingly beholden to the left. Shudder to think that in such an outlook the power behind the throne of a doddery Biden would be Kamala and her left wing BLM + Silicon valley + Hollywood + mainstream media PC camp.

Yes, and that is why so much political scuttlebutt is flying around that Putin is Trump’s lackey or the reverse, depending on the day.

It is laughable reverse political psychology in this case but the Dems continue to spread malarkey to the same crowd they trolled for over three years ckaiming that the Russian hoax was real. This time they are hoping enough of those gullible voters will elect “safe” Biden when as you indicate, he’s planning on selling the US down that Iranian river!

It wouldn’t surprise me if Biden wins and stupid Americans deserve it!

Good prognosis, Joel. One would have thought that if Biden were to win, pragmatism would prevail and the Green lunacy would be dumped after electioneering. But given the past few months of seeing the Democratic party in an ever further leftward drift, and given that the power behind the throne behind a doddery Biden presidency will be Kamala, your prognosis may well come to fruition, to the detriment of us all, American or not American.

Excellent prognosis — thank you Joel!

Supply and Demand. Preparing for reduced demand is a perfectly reasonable thing to do.

Electrical production should not be petroleum based. Automobile power need not be petroleum based.

Air transport and ocean transport will, in all probability, remain petroleum based — unless there is a real breakthrough in mini-nuclear power — after all, we have had nuclear submarines and aircraft carriers for some time now — but they are expensive.

Despite those obvious facts, there will remain all the rest of the demand for petroleum for manufacturing all the things we make from it.

Fracking will supply the world with sufficient natural gas to supply on demand electrical power re-purposing the old coal and fuel oil power plants.

Despite the glut of oil — gasoline prices remain, in my area, over US$ 2.00 per gallon.

Some thoughts on what you wrote:

While the US Navy nuclear reactors last for 30+ years in-service in the boats they are installed in, they are planned to run at operational power levels for probably only 1/3 of the time. This is due to being in port for half their life on a rotation basis with the fleet and in ready reserve to deploy under a crisis, and for periodic major overhaul-refits every 8-10 years that last 18-24 months each. You could never plan on a commercial generation reactor to have an out-of-service schedule like that.

No one is even contemplating what an aircraft reactor would look like since the early 60’s.

Ocean transport use is down sharply with COVID-19 reduction in supply chain demands…. and the big capacity hit that is underway in the Cruise line industry. That industry will likely never recover what COVID has done to it. All the Cruise lines are accelerating cruise ship retirements and dismantlement and planning on major cruise ship fleets size reductions. No one really knows what the cruise line industry will look like in 2 years when the COVID-19 pandemic is passed, but it surely will be at least at least 50% below 2019 levels. And that’s a lot of oil that won’t be burned, much to the Greens delight, and much to South Florida’s, and many small islands dependent on the tourist money they brought, economic detriment.

Places like Hawaii and most tourist dollar oriented island nations, where the cost of everything including electricity is already skyrocketing, can only get much worse in a less vacation travel-oriented world economy. And you simply cannot even think to build a small, modular nuclear reactor in most of those tropical places without much (irrational) fear from the locals. None of them want to blanket their limited spaces with solar panels (that don’t work at night anyways), or put up big ugly wind farms that corrode quickly in marine environments. So shipped in oil and/or LNG are their only energy options to live with a modern conveniences, like lights, TVs, clean water, treated sewage, and A/C where needed.

Gas in So Arizona is hovering right at $2.00/gal today. In many parts of Texas, Louisiana and the mid-west is is well below $2/gal already as the summer driving season is over, and much of the US economy is still idling (school buses not running much at all, and such).

“Automobile power need not be petroleum based”. But it does, at least for the next several decades. EVs make up about 1% of the automobiles on the road now and less than 1% of the miles driven. EVs make up about 2% of the new vehicles sold. The average age of a car on the road is approaching 12 years. You can expect that the 98% of light vehicles sold today that are powered by internal combustion engines will continue to be on the road for a decade or longer. The turnover rate for existing ICE cars is slow and the market penetration of EVs is currently quite low. Battery production is projected to limit the annual new vehicle market penetration of EVs to ~10% for the next 8 – 10 years – battery production capacity isn’t being built fast enough to sell more EVs than that in the next ~decade. That adds up to the fraction of light vehicles powered by petroleum being the majority of all light vehicles for decades to come.

The inflation-adjusted price of gasoline in the US was at it’s all-time low in 1998 at $1.60. It’s now $2.19. The inflation and tax adjusted price is even closer. This despite US gasoline demand having increased (even post COVID lock down) since 1998. $2.00 per gallon is cheap.

There are over 1 Billion vehicles in the world and the known global lithium reserves is only 8.6 million metric tons. If all vehicles were EVs, that would only divide out to 8.6 kg of lithium for each battery, whereas a typical Tesla EV battery has about 73 kg of lithium. This doesn’t even include all other Li-ion batteries and storage for renewables, so pray tell how auto power need not be petroleum based?

The manufacturing of 90 million BEV’s would consume 136% of the global proved reserves of lithium and 92% global proved reserves of cobalt.

https://wattsupwiththat.com/2017/10/31/wall-street-loves-electric-cars-america-loves-trucks-tesla-news-cobalt-cliffs-lithium-landslides-and-real-disruptive-innovation/

Hehe, break it out and pass it around, ya won’t have so much.

As an Albertan it sure would be nice to know the real intentions of a Biden toward energy and fracking

It all depends on who he is talking to I guess.

Energy independence for North America should be the goal of any Sane USA president.

Drove by a major pipe yard in eastern AB this week, for KXL, it’s been sitting there on hiway 570 for years, now almost empty

The pipeline is under construction just to the west of it.

Any bets on whether Biden will seriously kill the project?

There are lots of unionized construction workers busy on that

A President Biden would be controlled by the Left wing of the Democrat Party. At least until he is replaced by VP Harris via the 25th Amendment when his advancing dementia becomes too difficult to bear.

The Left wing of the Democratic Party is “shutdown all new and on-going oil and gas pipelines that cross state-lines or national borders.” Period. End of discussion.

Cheap natural gas is keeping electricity prices low and is killing the economic incentive for the wind and solar investments the GreenSlime is banking on for super-sized ROIs. Skyrocketing electricity prices is feature, not a flaw, of wind and solar energy.

And continued cheap gasoline is killing the rationale for Americans to buy EVs and then to buy that high priced electricity to charge their cars.

Of course he and Kamala will try. They pander to the unions but don’t actually help them much (except Obama cancelling school vouchers in Washington DC when he was president. Talk about hurting your constituents.) Dems correctly assume that the unions will continue to support them even though they do things that hurt the unions. The big exception was when West Virginia finally figured out that Obama was serious when he attacked coal and killed the state’s economy. Too late for them but at least they understood that this was a campaign promise that dems would keep.

Biden’s intentions – really that of Harris and all the Obama folks that will run the White House – are very very clear.

He/they will do everything they can -easily done through additional rules and regulations – to limit or cease fracking and/or oil/gas production.

Like all ideologues , what matters most is imposing their ideology upon the citizenry; EVERYTHING else is secondary or not important. If their policies are harmful to the citizenry or the nation , they do not care; they will demand the citizenry “tighten their belts” or “learn to code.”

If their policies once again make the USA dependent on foreign oil – as incredibly stupid this is – is of no concern to the Biden/Harris/Obama orbit. In fact, they would welcome this eventuality.

They will just maintain they are “saving the planet,” and spend billions on unreliable solar and wind facilities.

Biden and his ilk, by virtue of their wealth and influence are immune and exempt from any negative consequences their policies impose upon the citizenry.

As an analogy, while the average Cuban citizen waits on interminable lines for chicken scraps, Castro and his pals are living high on the hog.

For the ideologue, this is how it should be.

Their belief system and imposing it upon the “unwashed masses” (the Kulaks, the deplorables) is all that matters.

His intention is to gut all petroleum and coal production/use. He has said so for several years, repeatedly.

California Politicians are pragmatic. They legislated the production of low carbon fuels thinking cellulosic ethanol would be developed commercially. It wasn’t. But the lack of production means the state gets to add an extra tax to all the fuel that doesn’t meet that standard. I’m sure the clever politicians in California will find a way to tax vehicles with internal combustion engines to make up for the impractical aspirations of the green zealots.

They are only pragmatic in the sense that they make every effort to find new sources of revenue to spend and leaving no stone unturned in that search.

That “pragmatism” in finding OPM is driving a new and higher waves of wealth exodus from their state.

And just like a dam failure that exists for a long time as slow, steady trickle, the catastrophic collapse always accelerates exponentially near the end when it’s too late to stop it.

https://www.foxnews.com/opinion/ben-shapiro-leaving-california

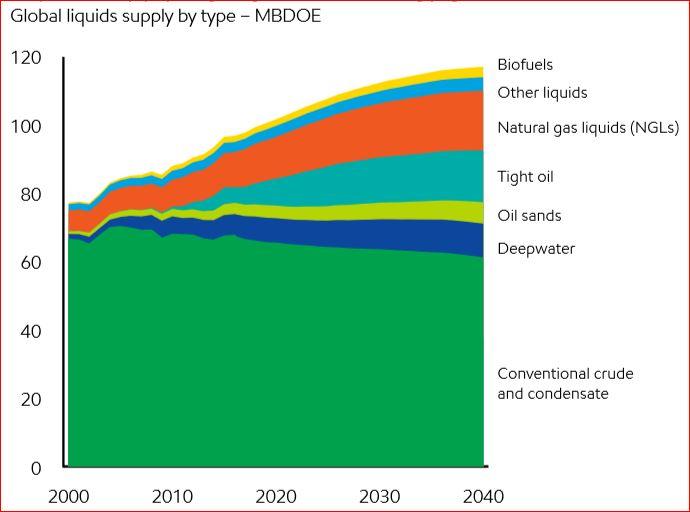

Conventional Oil peaked in 2006/2007 as shown by ExxonMobil Outlook 2019’s breakout of Liquids Supply p31.

i.e., Conventional Crude & Condensate and Deepwater oil production, excluding Fracking (“Tight Oil).

https://corporate.exxonmobil.com/-/media/Global/Files/outlook-for-energy/2019-Outlook-for-Energy_v4.pdf

Similarly in 2018

The entire Climate Scam foundation 20 years ago based on on your premise. That “peak oil” would deliver a fountain of money to renewables investors without any effort other than political-provided tax incentives early on to build them. The fracking revolution changed everything. Like nuclear energy power and bombs, the technology and methods can’t be “un-invented.” Fracking tight oil and gas will continue and grow as conventional oil continues to decline…. if the politicians stay out the way and let free markets work. Selecting the wrong political system could be a suicidal mistake that can’t be recovered from. Which of course is what the Left is banking on.

Political forces can act to throttle them both, nuclear power and fossil fuel power. Like all “good intentions,” maybe done for a seeming good, but if the applications are asymmetric with respect to East vs West, China vs the rest, Democracy vs. Totalitarian states, etc, the effects won’t be stabilizing, but exactly the opposite effect on world conflict.

So there is a real potential for the coming 21st Century conflicts, with the ascendancy of socialist political forces in the Western democracies, to make the major world conflicts and genocides of the 20th Century look like warm-up events. Choose the wrong political system, and they are all but assured.

Actually, we will be using more oil when the reality sinks in that policy failures produced lower growth than required to pay for all the giveaways and pay higher debt payments.

It’s difficult to figure how this will play out, especially with interest rates pretty close to zero and a lot of losses will be working their way through the system over the next year or two.

Then, perhaps even more crazy, a national moratorium on evictions for a year is a possibility. And suburban real estate prices our surging, while commercial real estate is doing the opposite. And a lot of government and private employees are being paid to sit on their assess.

You left out tax increases to stir the pot and spending that is over the top. We are dealing with prospective leadership that can’t see beyond cannabis and craft breweries for industrial strategy. The Chinese will fill all the voids and then some.

You left out the fact that half of the western world’s population is disconnected from reality lol. They are convinced every step of the way that new problems arising are the fault of the private sector and capitalists and that only government can fix them.

Also, there’s no such thing as, “clean energy.” They’re all dirty.

And as for [dirt/(kW-hr produced)], wind and solar are outstandingly productive.

It seems as BP and RD Shell are just collecting virtue bonus points by describing their economic adjustments as preparing for a transition in so-called sustainable energy generation.

The only current worthwhile transition is to fission power.

Funny thing… If you measured [dirt/(kW of coal replaced)], the results would be…

1. Nuclear

2. Natural gas, close second.

3. Wind, very distant third.

4. Solar, very, very, very distant fourth.

Reversed order?

The order is correct. The higher the capacity factor, the greater the reduction [dirt/(kW of coal replaced)]… Note I’m using kW rather than kWh.

Sorry, I guess I’m just having trouble conceptualizing those units, especially the kW of coal replaced. If I were feeling ambitious, I would collect and tabulate some typical numbers.

kW of coal replaced = kW of coal-fired electricity generating capacity replaced

If there is cost advantage to using oil for transportation that will benefit countries that do not sign into co2 agreements.

OR those who have exemptions like China, India and actual real 3rd world nations

An excellent blog – US under Trump has shown how the double works. The generation change to the use of natural gas for power generation and the rapid increase in energy availability through fraccing has led to the US outsripping its competitors in the capacity to provide cheap energy and to enhance global competition. As an aside the US has also managed to reduce CO2 levels where its woke competitors have failed dismally. Not a bad effort from the Land of the Free all said & done.

From the article: “Wood Mackenzie, a consulting company, estimates that there will be a net increase in global coal-fired power capacity this year, with 22 gigawatts of closures in Europe and the US more than offset by 49 gigawatts of plants opening in Asia.”

The Europeans are defiling their landscapes with windmills and solar, and bankrupting themselves, in order to cut their CO2 production, meanwhile, China and others are making the European reductions meaningless.

I guess the European politicians don’t realize how stupid they are acting and how ineffectual their actions to reduce CO2 really are.

Idiocracy in action.

This makes me wonder if much of the motivation for ME countries to suddenly be jumping on the Peace With Israel bandwagon comes from this veritable crash oil prices. Cutting the palestinians out of the process has allowed them to look at global realities and realize peace with Israel is good for the entire region, plunging oil prices may just have given them that little push needed to overcome decades hedging and sidestepping the real issues.

The Middle East oil producers have nothing to worry about long-term, because their oil is relatively cheap to extract, compared to oil-bearing formations in other countries. Even at reduced world prices, they can still make a profit on oil. The main problem for most Middle East oil producers is that their economies are very one-dimensional, since they have very few other industries and practically no agriculture, so they depend on oil revenues to buy other things their people need.

The decisions by Shell and BP to invest in “green” energy depend on government subsidies for such energy, and during a period of slack energy demand generally (right now due to COVID-19), governments will be questioning the wisdom of such subsidies when prices of gas- and petroleum-derived energy are relatively low, and social disruptions and unemployment problems created by COVID-19 need their attention.

Fracking for oil in the USA isn’t as profitable now (during the COVID-19 scare) as it was last year, but the last thing we need is for a Biden/Harris administration (or Harris/??? if Biden retires) to ban fracking. The COVID-19 scare won’t last forever, and if either a vaccine or effective therapeutics are developed soon, international tourism and trade will resume, and increase energy demand. This was true even after the Spanish Flu pandemic in 1918-1919, from which the recovery led to the “Roaring Twenties” economic boom under conservative President Coolidge.

The Trump policies of encouraging fracking and building oil pipelines made the USA energy-independent, so that we are no longer beholden to Middle East countries for oil. This may have helped the Trump administration negotiate peace deals between the UAE and Bahrain with Israel, as some Sunni Arab countries now consider Iran to be a bigger threat than Israel, which has not attacked any other countries in over 30 years (the UAE and Bahrain are geographically very close to Iran).

The current slump in energy demand due to restricted travel has an unbalanced effect on petroleum demand. Most of the drop in transportation demand has been air travel, which burns mostly kerosene. Automobile traffic (which burns mostly gasoline) has not dropped as much, and truck and freight rail traffic has remained fairly steady (which burns Diesel fuel).

Refineries that can crack heavy oil are adjusting their yields to prioritize Diesel over kerosene and gasoline, and favoring feedstocks that produce high Diesel yields, while their kerosene tanks are full to the brim, waiting for the airline industry to recover. The crude oil fracked from the Permian Basin and Bakken fields is generally light, producing more naphtha that can be refined into gasoline than heavier Middle East oil. Fracked American oil also tends to have less sulfur than Middle East oil, which make it easier to refine, reduces demand for hydrogen for desulfurization, and produces less elemental sulfur or sulfuric acid as by-products.

While the demand for fracked oil may be relatively low now, this source of energy should be kept operational for when demand for all petroleum products re-increases after the COVID-19 scare wears off.