Guest smack-down by David Middleton

Hat tip to Clyde Spencer…

The Oil Age Is Coming to a Close

Noah Smith

Bloomberg October 29, 2019(Bloomberg Opinion) — The oil industry faces an uncertain future. The world is rapidly waking up to the severity and immediacy of the threat from climate change. At the same time, electric vehicles are getting cheap enough to compete with internal-combustion engines. BloombergNEF expects electrics to begin taking over in about a decade:

[…]

Yahoo! Finance

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

Bloomberg

Which is it?

Does “the oil industry face an uncertain future”? Or is “the Oil Age coming to an end”? “The Oil Age is coming to an end” doesn’t sound very uncertain to me. Or maybe Former Professor Smith listened to too many Doors albums in college (I know I did)…

The future’s uncertain and the end is always near…

Jim Morrison, The Doors, Roadhouse Blues, 1970

Before “electrics begin to take over,” they first need to top Ford F-Series pickup trucks.

EV’s may be taking over in the parking lots of the ivory halls of academia and LaLa Land of BNEF blogging, but the developing world likes SUV’s.

Oct 23, 2019

SUVs: A Reality Check On Oil Use And CO2 EmissionsJude Clemente Contributor

Energy

I cover oil, gas, power, LNG markets, linking to human development.The never-ending spirit of wanting a more enjoyable and easier life is a constant reality that far too many of us involved in our energy-environment discussion unwisely choose to ignore.

A perfect example of this is SUVs: gas-guzzling Sport Utility Vehicles that are increasing both oil demand and CO2 emissions.

Much bigger, much safer, and much more fun to drive, the harsh fact for some is that people love SUVs.

The Paris-based International Energy Agency gives us a much-needed reality check on SUVs, oil demand, and the corresponding CO2 emissions.

SUVs are becoming more popular in the emerging economies of the world, where urbanization and expanding middle classes are giving more people more access to buy.Many see SUVs as a symbol of wealth and status.

And why not?

Even environmentalists Alexandria Ocasio-Cortez and Mayor De Blasio love oil-swilling SUVs.

[…]

Forbes

Jude Clemente actually understands the energy industries… as opposed to the to the former professor of finance, who seems to be clueless about… everything…

Meanwhile, concerns over groundwater pollution are leading to growing calls for a ban on hydraulic fracturing, the main source of increased U.S. production during the past decade.

Former professor of finance

The former professor of finance is almost half right. Frac’ing is the leading “source of increased U.S. production during the past decade.” The second-leading source is the deepwater of the Gulf of Mexico, where “shale” scale frac’ing isn’t a factor (1)(2)(3).

However “concerns over groundwater pollution” are only “leading to growing calls for a ban on hydraulic fracturing” from left-wing (Marxist) politicians. There is no evidence whatsoever that frac’ing is any threat to groundwater.

Can anyone guess how many times I’ve heard this sort of thing the past 38 years?

Reduced demand for crude will send prices plunging, cutting into profits at oil extractors and refiners. Share prices of oil majors have drifted lower in recent years:

[…]

Workers in the energy industry need to be prepared for this shift. For knowledge workers, such as geologists, chemists and software engineers, this means cultivating technical skills that can be useful in other fields such as information technology, pharmaceuticals, health care or finance.

Former professor of finance

Clearly, this former professor of finance doesn’t know Jack Schist about the oil industry. The oil & gas business follows a “boom & bust” cycle. High oil prices reduce demand relative to supply. Low oil prices reduce supply relative to demand, ad nauseum. Shares of most oil companies have been beaten down since 2014-2015 because the price crash destroyed a lot of equity. If “reduced demand for crude” sends “prices plunging,” it will spur an increase in demand. That’s how business works. Maybe they don’t teach this in former professor of finance school.

While the oil industry certainly employs some chemists and software engineers (although, I’ve never worked for a company that did), the “knowledge workers” primarily consist of petroleum engineers, geologists, geophysicists, accountants, lawyers, petroleum land management professionals and compliance specialists. At least he mentioned geologists. Cyclical downturns have led to several episodes of layoffs since 1986 and the voluntary exodus of many “knowledge workers”. Most of the geoscientists (geologists and geophysicists) I started out with at Enserch Exploration in 1981 left the industry in the late 1980’s through 1990’s. Most went into hydrology/environmental/engineering geology, a few became schoolteachers, one became a NASA astronaut and is currently the Director of the USGS. I know of maybe 2 or 3 who went into finance… And none who went into pharmaceuticals or health care. Otherwise, no schist Sherlock… Back up plans are sort of de rigueur in this business.

This is where the former professor of finance went full Tropic Thunder.

Lower-skilled workers and fracking boom towns, however, will have a much harder time landing on their feet.

[…]

The problem will be compounded for those who live in the small towns and cities that grew up around oil-extraction sites. Americans have been less willing to move from place to place in search of work in recent decades, and big cities are no longer lands of opportunity for those without an advanced education. The decline of the oil industry may leave the country dotted with yet more decaying half-empty ghost towns, unable to pay for the upkeep on their infrastructure, afflicted with drugs and alcoholism and suicide.

Governments at the local, state and federal levels should work to prevent this unhappy future. People in decaying oil towns can be given vouchers to help them to move, perhaps to a nearby thriving college town.

Former professor of finance

Did I mention that this former professor of finance doesn’t know Jack Schist about the oil industry? What does he think Houston, Midland, Tyler and a whole lot of other oil towns looked like in the late 1980’s, early 1990’s and other bust cycles?

Did he seriously suggest giving hard-working blue collar workers “vouchers to help them move to… a nearby thriving college town”?

But… Then he sped right on past full Tropic Thunder.

The march of technology means oil’s days are numbered.

Former professor of finance

The oil industry is a helluva lot more high tech than wind and solar. Due to advances in seismic imaging technology over the past 40 years, we can literally “see” oil & gas accumulations more than 30,000′ below sea level in geological settings that couldn’t even be imagined, much less imaged, just 10 years ago. Due to advances in drilling technology, we can now drill highly precise directional wells in over 10,000′ water depths, through thick layers of salt, to hit pinpoint targets we didn’t even know were there just a few years ago.

The “march of technology” means that “oil’s days are numbered in decades, if not centuries.

I have read a lot of truly idiotic articles about the demise of the oil industry, often sponsored by Bloomberg New Energy Finance, but this one takes the cake. The former professor of finance earns a Distinguished Ron White Cross with a The Stupid it Burns Service Device and a Billy Madison Lifetime Achievement Award…

Technical, facts, etc…

“You Keep Using That Word, I Do Not Think It Means What You Think It Means” – Inigo Montoya

a) Society is outlawing fossil fuels

No, society is not (as evidenced by the fact that they continue to use the stuff in great quantities). Politicians of certain political persuasions are certainly trying. politicians do not equal society.

b) There are good reasons for that

No there really isn’t. But do enlighten us, what are these “good reason” you think exist.

c) A new energy source from atomic hydrogen exists and many companies are working on it.

great, where can we see it in action. A real working commercial operation. What’s that? there are no working commercial operations? then you are at best hyping prematurely at worst hawking snake oil. Judging by your posts thus far its definitely the later, and as I said no one’s buying.

d) The large asset managers are transitioning away from fossil fuel investments

which, again, is meaningless. They’re not transitioning away because fossil fuels are bad investments, they’re transitioning away to show how virtuous they are about “saving the planet”. And remember you can’t sell your stocks with out there being willing buyers to buy it up.

e) With higher energy density sources than fossil fuels

Sounds great, Let’s see the real world commercial operations. Oh, that’s right there aren’t any.

Am I talking my book, of course!

About the only honest thing you’ve said so far.

If you have something to contribute professionally we can talk more

How about do you have something relevant to contribute to the subject of David’s post that you’ve been hijacking for your infomercial? thought not.

D. Investment is leaving for places where there are few or no restrictions on venting and flaring.

Or where there is high demand for natural gas at a high enough price that it is conserved.

The shallow gas industry in Alberta might have made money once. Once.

I thought you didn’t do predictions?

Regarding your first prediction…once again, you report an EIA long-term modelling projection as though it has any semblance to future reality. You appear completely unable to distinguish reality from the “fantasy land” (your words) that the EIA long-term modelling team occupies. Virtually everyone who is knowledgeable about the subject agrees that the future of light duty vehicle transportation is by autonomous electric vehicles, operated by fleet owners in mobility-as-a-service mode.

https://www.cnbc.com/2017/11/07/former-gm-vice-chairman-bob-lutz-self-driving-cars-will-take-over.html

https://www.mckinsey.com/~/media/McKinsey/Business%20Functions/Sustainability/Our%20Insights/An%20integrated%20perspective%20on%20the%20future%20of%20mobility/An-integrated-perspective-on-the-future-of-mobility-article.ashx

https://www.forbes.com/sites/energyinnovation/2017/09/14/the-future-of-electric-vehicles-in-the-u-s-part-1-65-75-new-light-duty-vehicle-sales-by-2050/#76551c18e289

https://www.globalxetfs.com/future-of-transportation-is-autonomous-electric/

https://www.disruptordaily.com/future-of-transportation/

So do you wanna bet that “Ford F-series (gasoline) pickup trucks will still be outselling all EV’s (sic) in 2050″? I’ll give you 20-to-1 odds on up to a $20 bet.

Regarding your second prediction…”…if not centuries”?! C’mon! You apparently don’t even have the slightest idea what transportation will look like in 2050 (see your first prediction)…so what in the world makes you think you have any idea what transportation and oil use will look like in 2100, 2150, or 2200?

Do you seriously think that anyone in 1919 would know what transportation would look like even in 1969, let alone 2019 or 2069?

P.S. But as long as you’re now making predictions for “decades, if not centuries” into the future, what is your prediction for what year U.S. coal-fired electrical generation will go below 1000 thousand GWh…the bottom of your “Coal keeps on chugging away” graph?

https://markbahner.typepad.com/random_thoughts/2018/02/whos-in-fantasy-land.html

The “march of technology” means that “oil’s days are numbered in decades, if not centuries… Is not a prediction. It’s a bleeding obvious statement of fact.

The “march of technology” is the reason why every “end of oil” prediction has been wrong and will remain wrong for decades, if not centuries.

(Need to make a decision, can’t have this fine comment sit here) SUNMOD

Mark,

I think David is on solid ground regarding the future of the oil industry.

I read through your links and noted there were a lot of assertions, but very little in the way of data or logic to support the assertions. I agree with you that autonomous vehicles and transportation as a service (TAAS) will come to dominate the vehicle market. However, an autonomous vehicle can be powered by anything; batteries, an internal combustion engine, fuel cell, or even compressed air. Whether electric or internal combustion vehicles dominate the future market comes down to economics and project execution capabilities, and I believe we can make a fair estimate of this.

Assumptions:

1. There will be no Idiot Swan events. There will be no outright bans on drilling or frac’ing. Tax policy will not provide heavy subsidies for renewable power or batteries, nor will tax policy unduly burden oil and gas production.

2. The difference in purchase price for an EV and ICE vehicle will be almost immaterial to the economics of vehicle choice. This is based on the assumption that TAAS will push vehicle lifetime mileage closer to 1,000,000 miles, at which point the dominant economic driver will be fuel cost.

Vehicle Fuel Cost:

Based on today’s cost of gasoline and electricity (my latest bill) the cost of each at the wheel is:

• Gasoline: $0.3415/kWh ($2.50/gallon, 20% efficiency)

• Electricity: $0.2667/kWh ($0.16/kWh, 60% efficiency)

(efficiencies from your link https://www.forbes.com/sites/energyinnovation/2017/09/14/the-future-of-electric-vehicles-in-the-u-s-part-1-65-75-new-light-duty-vehicle-sales-by-2050/#76551c18e289)

This places gasoline at a 30% price disadvantage relative to electricity (not the more than 2:1 price disadvantage in your link https://www.globalxetfs.com/future-of-transportation-is-autonomous-electric)

So if fuel cost for an electric vehicle is lower and the initial purchase price differential is assumed to not be a factor and TAAS effectively eliminates the charging management and range issues that affect EV acceptance, then why do I believe the EV’s will not take over the world anytime soon?

Simple. I have reason to believe that the cost of electricity will rise both because of rising demand and the move to renewable power generation. I also have reason to believe that the availability of electricity will be a constraining factor; we just can’t build it fast enough.

The Future Cost of Electricity:

Moving to 100% renewable electricity power generation will considerably increase the cost of electricity.

The installed cost of solar PV, wind, and for comparison combined cycle natural gas turbines (CCGT) are:

• Solar: $3,000/kW (multiple sources)

• Wind: $1,400/kW (https://www.conserve-energy-future.com/windenergycost.php and

https://www.wind-energy-the-facts.org/index-43.html )

• CCGT: $965/kW (EIA)

Of course to get the costs on a consistent basis we should include the cost of fuel for the expected life of the shortest lived capital investment, estimated at 20 years.

• Natural Gas NPV: $3,108/kW ($4.00/MSCF 2019 pricing from EIA, 2.5% interest rate)

This yields an equivalent installed cost for a combined cycle natural gas turbine of $4,073/kW.

So it appears that renewables really are cheaper, quite a bit cheaper, than all the other power sources. Could the proponents of renewable power be right?

No. We all know that we have to look at what it costs to provide reliable 24/7/365 power, which is a vastly different proposition than installing ‘nameplate’ power. To supply reliable power requires the installation of additional solar PV or wind turbines to produce enough power above immediate consumption to meet 24/7 power demand and batteries and inverters to store the power until needed. So we need installed cost for inverters and batteries:

• Inverters: $392/kW (National Renewable Energy Laboratory: “2018 U.S. Utility-Scale

Photovoltaics-Plus-Energy Storage System Costs Benchmark”)

• Batteries: $73/kWh (Also from “The Future of Electric Vehicles”, 2030 estimated

cost)

Based on this the estimated installed cost to deliver 1 kW of power continuously is:

• Solar: $17,792/kW

• Wind: $11,246/kW

• CCGT: $ 4,244/kW

Assumptions:

• Solar: 8 hours minimum daylight in winter, no more than 1 day without sunlight, and 2 days to recharge after discharge.

• Wind: Average generation at 30% of nameplate, no more than 1 day without wind, and 2 days to recharge after discharge.

• CCGT: 85% mechanical availability.

Obviously how you play with the assumptions has a huge impact on cost. For solar I assumed a southwest desert climate with relatively long winter days and short periods without sunlight. Similarly for wind I assumed nearly continuous wind as one would expect in the mountain west.

What’s driving the cost is the need to install 5+ kW of nameplate capacity plus 40+ hours of batteries to support 1 kW of reliable 24/7/365 power. Costs escalate precipitously for conditions in the northeast (less sunlight, less wind). This is just a hugely inefficient use of capital (but an interesting spreadsheet exercise.)

Based on the installed cost we can estimate consumer power cost:

• Solar: $0.4059/kWh

• Wind: $0.2566/kWh

• CCGT: $0.0486/kWh

I’ve assumed a 5 year simple payout on capital invested. The fuel component of the power cost for the CCGT is the price of natural gas prorated for turbine efficiency of 60%.

When we including delivery charges we get a total cost of:

• Solar: $0.4959/kWh

• Wind: $0.3466/kWh

• CCGT: $0.1386/kWh

I chose a flat $0.09/kWh based on my power bill. This is likely underestimated in all cases as I would expect solar and wind to have higher delivery costs due to the geographically diffuse nature of the systems and the CCGT cost excludes natural gas delivery to the plant.

Vehicle Fuel Cost in a Renewable World:

The cost of power at the wheel again assuming 60% conversion efficiency in an EV.

• Solar: $0.8265/kWh

• Wind: $0.5777/kWh

• CCGT: $0.2310/kWh

• Gasoline: $0.3415/kWh

As we can see solar and wind are not at all competitive with gasoline, running respectively 242% and 169% relative to the price of gasoline. This is not going to incentivize anyone to buy electric cars; certainly not fleet owners. However we can see that natural gas retains a strong economic advantage over gasoline and assuming suitable supplies could support the conversion to electric cars.

The Future Cost of Gasoline:

Should electric vehicles start to reduce the demand for oil I would expect to see the price of gasoline drop, potentially quite a lot. On the low side the price of oil is limited by the cash flow requirements to keep production going. In refining margins would drop through cost cutting and the closure of high cost/bbl refineries and is limited by cash flow requirements. Speculating here but in dire circumstances gasoline prices could drop to between $1.00 and $1.50/gallon.

The one thing we can say with reasonable certainty is that the supply of oil will be adequate for the next several decades. Therefore the cost of gasoline is not likely to rise precipitously and drive the economics toward electric vehicles.

Converting Transportation to Electricity:

What I never see mentioned is what it will cost to convert all the fossil fuels used in transportation to renewable electricity. Does nobody think about these things?

Thinking about it, in 2016 fossil fuels used for transportation represented 26.44 quads of energy (EIA). To put this in perspective fossil fuels represented 23.54 quads to electricity generation; transportation and electricity generation consume about the same amount of fossil fuels. The total fossil fuel contribution to electricity generation and transportation comes in at 49.98 quads. The cost to convert this infrastructure to renewables is (in $Trillions):

Transportation Electricity Total

• Solar $15.73 $14.00 $29.73

• Wind $9.94 $8.85 $18.79

These numbers exclude distribution costs and EV support infrastructure costs. If we call this an additional 25% to 50% above solar or wind installation costs then we are talking in round numbers $24 to $44 trillion. To put this in perspective the GDP of the US in 2018 was $20.5 trillion. To eliminate fossil fuels in transportation and electrical power generation by 2050 we need to invest $1 – 1.5 trillion every year, or 5-7.5% of the US’s GDP. (Note that this excludes nuclear and fossil fuels used by industry.)

Another way to look at this is we need to execute 1,000 – 1,500 separate billion dollar projects every year. My personal experience with multi-billion dollar projects is they take 8-10 years to execute and finding qualified people is like finding hen’s teeth. The management, engineering, and skilled trade resources are just not out there to execute in effect 10,000 separate billion dollar projects in parallel for 30 years. (Finding qualified people for a multi-billion project during the financial downturn in 2008-2010 was just about impossible.) Finally, if we were to try the competition for resources would drive engineering and construction costs up tremendously.

Wrapping Up:

Oil will remain the primary transportation fuel for the next several decades. While a superficial look at today’s prices for electricity and gasoline seem to indicate a strong economic driver for converting automobiles from internal combustion to electric a deeper look at the probable future cost of electricity versus gasoline shows a strong economic advantage for gasoline over electricity derived from renewable sources. Electricity sourced from natural gas (combined cycle gas turbines) retains an economic advantage over gasoline and assuming suitable supplies exist could support the conversion to electric cars.

Regardless of economics the large cost and skilled labor demands of converting the economy to renewables makes it highly unlikely that a significant portion of the fossil fuel supplied portion of the transportation market can be converted to renewables by 2050. Even if we limit the project scope to using natural gas derived electricity to support the conversion to battery powered cars limited management and technical resources will likely constrain the pace of the conversion.

[This should be made full posting, and not just a comment. Mod]

[Concur. .mod]

David wrote, “Looks like Ford F-Series pickup trucks will still be outselling all EV’s in 2050. (US Energy Information Administration)”

Do you think he is on “solid ground” with that statement?

I thought you didn’t do predictions?

Mark you are being dishonest. you selectively quoted to get that first prediction, here is the full quote:

Drat, messed up the html tagging everything starting with “note the parenthetical” should be outside the blockquote, thusly:

note the parenthetical – it’s an observation based on the data provided by the EIA, David’s not the one making a prediction here, EIA is. Since you were caught in a blatantly dishonest comment right at the start of the post, I didn’t bother reading any further as life is too short to waste it reading the babblings of obvious liars.

You quoted David Middleton:

And then you state:

If David doesn’t know that the EIA’s projection of EV sales in the U.S. in 2050 is utter rubbish, he is ignorant. If he does know that the EIA’s projection of EV sales in the U.S. in 2050 is utter rubbish, then he is being dishonest if he writes, “Looks like Ford F-Series pickup trucks will still be outselling all EV’s(sic) in 2050…” even if he includes the parenthetical.

So either he is ignorant about likely EV sales in the U.S. in 2050, or he is being dishonest. (Or perhaps both.) Take your pick.

Yes, the same thing could have been said in 1909 about the age of the horse. If someone had said in 1909, “horses’ days are numbered in decades, if not centuries” it would have been a “bleeding obvious statement of fact”…which would provide absolutely zero useful information about the future.

So congratulations, David. Another statement that provides absolutely no useful information about the future. Just like your statement that “Coal keeps on chugging away”…apparently, there’s absolutely no set of future events that will cause you to acknowledge that was incorrect.

But what about you claim that it, “Looks like Ford F-Series pickup trucks will still be outselling all EV’s in 2050”? Was that also a “bleedingly obvious statement of fact”? Or a prediction?

P.S. And I’m still waiting for your prediction of what year U.S. coal-fired electrical generation will go below 1000 thousand GWh…the bottom of your “Coal keeps on chugging away” graph that extended out to 2050 with a plateau above 1200 thousand GWh. (Note: This fact may not have reached the “fantasy land” in which you live, but coal-fired generation was *below* that 1200 thousand GWh level *last year* in the U.S. I’d say that’s a bit before the year 2050, wouldn’t you?

Unlike babbling idiots, I don’t do predictions.

Exactly which advances in technology made horses invalidate constant predictions of their demise?

Wake me up when it looks like US EV sales will overtake Ford F-Series pickup trucks.

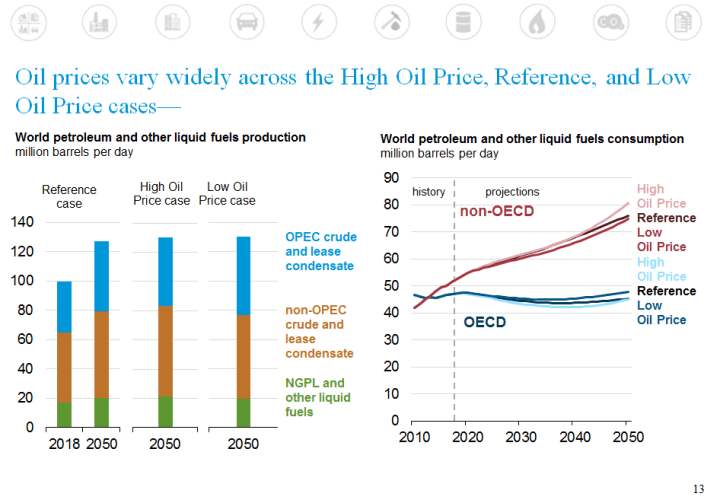

The math doesn’t get much better for EV’s when non-OECD nations are included…

Part 1

Yeah, right. You take the EIA’s already ridiculous projections, and add your own facile and obviously erroneous analysis, to come up with:

Please feel free to delete these improperly formatted comments. (My email program on which I composed them changed the closing “/blockquote” to “/blockbuster” and I didn’t catch the error.)

The previous incorrectly formatted comments can be entirely deleted, and substituted with:

Part 1

Yeah, right. You take the EIA’s already ridiculous projections, and add your own facile and obviously erroneous analysis, to come up with:

It looks like that to you, does it? That’s because you’re one monumentally ignorant and analytically incompetent twit. I’ll give you $100 if you can find anyone with an engineering degree who has ever spent even 1 year at a company that makes autos who will come here to WUWT and state for the record that he or she thinks there is even a 50/50 chance that “Ford F-series gasoline and diesel pickup trucks will still be outselling all EV’s in the U.S. in 2050.” And I’ll also simultaneously donate $100 to the charity of your choice if you find person. And I challenge you to offer me even $10 (up to $50) for every person with an engineering degree who has worked at least year at an auto company who thinks there’s less than a 50/50 chance. And I’ll donate another $50 to the charity of your choice if you make that offer.

You obviously think you’re hot stuff. I think you’re a profoundly ignorant partisan hack. And dishonest to boot. And based on your analysis above that related to your claim about EVs in 2050, I don’t think you could perform a decent technical analysis of likely future U.S. light duty vehicle sales trends if your life depended on it.

Fortunately, we have a way to determine whether you know what you’re talking about, or whether you are an ignorant, dishonest, and analytically incompetent partisan hack, as I think.

1) I will give you 50-to-1 odds on a bet up to $20 that U.S. light duty EV (that’s BEV plus PHEV) sales will exceed Ford F150 (gasoline and diesel) truck sales before 2050. That means that if you bet $20 and light duty EV sales do exceed F150 gasoline/diesel truck vehicle sales before 2050, you give me $20. But if you bet $20 and I lose, I’ll give you ***$1000***. Further, to show my good faith, I’ll send you whatever amount you bet when we agree on the bet. So you’ll just send my money back plus whatever amount we bet if–actually WHEN–you lose. Further, if you even make this bet, I’ll give $100 to the charity of your choice.

2) I will give you 4-to-1 odds on a bet of up to $50 that U.S. light duty (BEV plus PHEV) sales will exceed Ford 150 gasoline and truck sales before 2035. I’ll do the same good-faith arrangement described above for this bet. And if you even make this bet, I’ll give $50 to the charity of your choice.

How about it? Feelin’ lucky, punk?

P.S. In Part 2, I will make you more fabulous offers. If you accept them, they might even educate you. If you’re capable of being educated.

Part 2

I will send you (or the charity of your choice) $10 for every one of the following questions you can answer correctly, up to $100. (I’ll be the judge of whether your answers are correct, but I’ll accept binding arbitration if we can mutually agree on an appeals judge.) However, I will only send you $10 for every correct answer if you try to answer all parts of all the questions. On multiple-part questions, I’ll give you $10 if you answer as many or more parts correctly than you answer incorrectly. Further, for every question you answer correctly, I’ll give a further $10 to the charity of your choice, up to an additional $100.

1) On page 128 of the EIA summary of AEO 2019, hyperlinked below, what is the Reference case estimate for U.S. EV sales in 2025? What were U.S. Ford F-series sales in 2018? What is the slope of the regression line, in F-series units per year, in your analysis of recent F-series truck sales? If one extrapolates from 2018 to 2025 using that slope, what number is obtained for F-series sales in 2025? Which number is greater, the EIA’s AEO 2019 Reference case estimate for EV sales in 2025 or the calculated value for F-series sales in 2025?

https://www.eia.gov/outlooks/aeo/pdf/aeo2019.pdf

2) Who is Mark Reuss? Do you think he knows more about potential trends in future auto/truck sales and technology than you? What has he said about the future of EVs?

3) What were GM’s approximate U.S. vehicle sales in 2016, 2017, or 2018? How do total GM vehicle sales compare to Ford F-series sales in the same year?

4) Can you name at least two auto companies with a market cap above $10B (other than Tesla) that have publicly announced long-term plans to produce exclusively electric vehicles?

5) From the EIA AEO 2019 summary below: For the reference case, what are the projected number of light duty vehicle sales in 2018 and 2050? What are the projected percentages of trucks in 2018 and 2050? Of the “trucks,” what percentage are large pickup trucks in 2018 and 2050? What are the EIA’s projected Reference case PHEV and BEV (you know what those are, right?) sales in 2050?

6) Based on your answers to question #5, and any other data you think are appropriate, what do you calculate will be the number of F-series trucks sold in the U.S. in 2050? Compare this number to the EIA’s estimate the total number of PHEV and BEV vehicles sold in 2050. You must show your work for credit.

7) From the Bloomberg NEF blog post, “A Behind the Scenes Take on Lithium-ion Battery Prices,” what is the approximate cost of an EV battery pack in 2018? What did BloombergNEF estimate would be the cost of a battery pack in 2024 and 2030?

8) From the graph below, what gasoline cost ($/gallon) is comparable to the EV battery pack prices for 2018, 2024, and 2030 from question #7:

9) What percentage of new global vehicle sales does Bloomberg NEF estimate will be electric in 2040?

10) What did Bill Ford of Ford Motor Company say at the Detroit Auto Show in January 2018 about Ford investment in electric vehicles, and the number of EV models Ford plans to have by 2022?

11) Does Ford plan to introduce an HEV and/or BEV version of the F150 pickup truck?

https://www.eia.gov/outlooks/aeo/pdf/aeo2019.pdf

The link above is what was referred to in question #5: “From the EIA AEO 2019 summary below…”

https://www.eia.gov/outlooks/aeo/pdf/aeo2019.pdf