In the past decade, since the release of the flawed 1998 study by Michael Mann, now known as MBH 98, the phrase “hockey stick” has been used to describe a certain shape of a graph. It has also become synonymous with poor data selection and bad statistical procedure.

Yet again and again we see climate studies pushing this hockey stick shape as a way of saying we are “living in the worst time period of the data”.

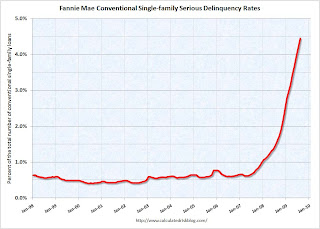

Here, without statistics, without bristlecone pines, inverted lake sediments, midge larvae carcasses, larch trees in Yamal, or convoluted never before seen statistical methods, I present a directly measured data set that produces a real “hockey stick” shape.

The data is directly measured and not a proxy, the plot is real. There’s no data adjustment or statistical manipulation. Care to know what it is?

From the website “Calculated Risk“

Here is the monthly Fannie Mae hockey stick graph …

Click on graph for larger image in new window.

Fannie Mae reported today that the rate of serious delinquencies – at least 90 days behind – for conventional loans in its single-family guarantee business increased to 4.45% in August, up from 4.17% in July – and up from 1.57% in August 2008.

“Includes seriously delinquent conventional single-family loans as a percent of the total number of conventional single-family loans. These rates are based on conventional single-family mortgage loans and exclude reverse mortgages and non-Fannie Mae mortgage securities held in our portfolio.”

Just more evidence of the growing delinquency problem, although these stats do include Home Affordable Modification Program (HAMP) loans in trial modifications.

Now that’s a hockey stick to be worried about.

It hardly is a surprise then that when we see that sort of graph of actual data in the American economy, we start to see graphs like this one depicting confidence in climate change as an important issue:

Source: Pew Poll, story here

(h/t to WUWT reader Michael)

Wow. The mortgage crisis ain’t exactly over.

What helter-skelter

Barney Frank and Boston Fed.

So, gimme shelter.

===========

No, no it is not. Housing prices will continue to have downward pressure on them because wages and employment are not recovering. Can’t buy a house (anymore) without any money.

I think the parallels between economic modeling and climate modeling are too richly ironic to ignore.

Both are subject to confirmation bias and popularity-based promotion. Tell people what they want to hear based on your model, and you are praised; tell people what they don’t want to hear and you are scorned and derided.

Both take chaos-rich systems and reduce them to a few simplistic explanations, which work perfectly for a while and then do not work at all once conditions morph beyond the bounds of the original model.

Both are used to drive policy, gaining influence far beyond their intrinsic worth.

Large amounts of money follow the popular projections, and then the money vaporizes. Those who promoted the models are not held accountable for the consequences of people taking them seriously.

Anyone else find this all a bit scary and foreboding?

It’s the ECONOMY, stupid!

IWWTWT

IT’S WAY WORSE THAN WE THOUGHT!!!!

but to be expected when politicians and Gubmint are involved!!!

No, Frederick, it’s a long ways from over. Not quite as big as the when the Savings & Loans went belly up but, still, big. Sad thing is both financial messes were predictable and primarily caused by government.

Funny, I was guessing that the graph represented the accelerated use of faked data by our friends, the warmists.

The Center for Responsible Lending estimates that there will be “13 million defaults over the time period 2008Q4 to 20014.” That is their estimate of “foreclosures on all types of mortgages.”

It’s doubtful if we are even halfway through the mortgage crisis.

The worse is yet to come. The time bomb hasnt even gone off yet. Hyperinflation will be coming soon.

I see you’ve identified a new proxy to be used in the next round of spaghetti graphs – I wonder if they’ll credit you?

As a renter who has never taken out a mortgage, I am not too worried about your hockey stick.

I am more worried about this one:

http://www.chartingstocks.net/wp-content/uploads/2009/03/money-supply.gif

A graph of FDIC bank closures will have the same shape (with no leveling).

Sunfighter (20:48:25) :

The worse is yet to come. The time bomb hasnt even gone off yet. Hyperinflation will be coming soon.

It’s not quite a true hockey stick shape, but probably a much more frightening graph. From the St. Louis Fed, the adjusted monetary base since 1910

http://research.stlouisfed.org/fred2/series/AMBNS

“The Center for Responsible Lending estimates that there will be “13 million defaults over the time period 2008Q4 to 20014.” That is their estimate of “foreclosures on all types of mortgages.”

It’s doubtful if we are even halfway through the mortgage crisis.”

20014 is a long time away. If we only have 13 million defaults by then we’ll be just fine…

I’m really glad you posted this one!

Now that they are realizing their climate hyperbole isn’t productive lets have something to be really scared of, and here it is, right before Copenhagen!

And Bush started warning of this problem in 2001 but Democrats in Congress and Senate Democrats (using the filibuster) in particular blocked any action. They went so far as to say in Congressional testimony that the problem was a figment of the Republican imagination.

There is a lot of testimony where Democrats are upset at Republicans for even calling attention to the problem.

They were warned going back to 2001 that this was going to happen. They chose to stick their head in the sand.

It is the same thing that is going on right now with climate “science”. They believe what they want to believe, facts be damned.

Anyone here live in California? Starting Monday you are going to find a surprise in your paycheck. The state government has decided that they are entitled to withhold more from your pay than is due in taxes in order to give themselves an interest free loan. They simply decided to take more of the people’s paychecks … which they might or might not be able to repay at the end of the year. And it is NOT voluntary. Anyone subject to withholding in California is going to have more withheld than is actually due. They believe your paycheck really belongs to them. We need to get rid of these idiots at EVERY level of government, municipal, county, state, and federal and get some people into office that know how to say “no” when it comes to the spending (and outright grabbing) of the people’s money.

I am so angry I could spit.

I meant to add that from Aug 08 to Sept 09 the economy was contracting sharply, so that 109% increase in the money supply was almost entirely the result of the fed printing money.

Here’s a similar post you guys might like. Briffa posted a sensitivity test reply to Steve McIntyre’s latest where he substitutes a bunch of other data with Yamal and still get’s hockey sticks.

Well rascal that I am I used his data and made my own versions of Yamal.

http://noconsensus.wordpress.com/2009/11/01/fixing-briffas-latest/

Bravo! Bravo! Direct, succinct, measured data for once! I am enthralled!

I am not so enthralled that is the ‘rate of serious [mortgage] delinquencies’, however. Be that as it may, it nice to see such a straight-forward presentation for once (not that there is anything wrong with that, or any deviation from that by the Team, the Team’s representatives or the Team’s duly deputized proxies for that matter) …

.

.

.

It’s sounds so good to let people who aren’t ready for a house loan to get one anyway with no money down, and then when they get in serious arrears on the payments, because they had no experience with handling money in that way, to offer them a re-worked loan. It sounds so nice to get as many people as possible in to their own house. But nice ideas don’t always work in the real world.

Nice ideas of benevolence create nightmares in the real world sometimes!

Anthony Watts,

Thank you for caring and putting this graph up as a post. I’m glad that more people are being made aware of this.

It may be a long road out of these troubles America has put itself into. But there is a better day on the way!

crosspatch (21:13:30) :

Anyone here live in California? Starting Monday you are going to find a surprise in your paycheck. The state government has decided that they are entitled to withhold more from your pay than is due in taxes in order to give themselves an interest free loan. They simply decided to take more of the people’s paychecks … which they might or might not be able to repay at the end of the year. And it is NOT voluntary. Anyone subject to withholding in California is going to have more withheld than is actually due. They believe your paycheck really belongs to them. We need to get rid of these idiots at EVERY level of government, municipal, county, state, and federal and get some people into office that know how to say “no” when it comes to the spending (and outright grabbing) of the people’s money.

As I understand it quite a number of those old oil platforms off the California coast are sitting on top of already drilled wells that have been capped. At any point, now or in the last 20 years, they are a month or two away from producing large quantities of oil. The royalties and taxes from them could or would have provided significant relief to California taxpayers and national relief for our imported oil bill. Given that studies I saw earlier in the year indicate that the predominate source of oil contamination in the oceans is now from sea floor seepage and pumping the wells might in all probability lead to a decline in oil pollution off the California coast, you might want to ask your legislators what they’re waiting for. Although at this point giving them more revenue to dispense is probably analogous to giving heroin to an addict.

That is a song I have been singing for quite a while. More oil seeps naturally from Coal Oil Point into the ocean in one year than was spilled by all offshore drilling operations in the decade of the 1990’s.

I also have a dear friend whose mother is in her 90’s. Her mother spent the summer in Santa Barbara. She said that before offshore drilling started, the beaches were foul with tar and the air smelled like kerosene. Her mother made the kids wash their feet in turpentine before they were allowed back in the house after going to the beach.

She said drilling did more to clean up those beaches than anything else.

“Her mother spent the summer in Santa Barbara.”

Meant: “Her mother spent her childhood summers in Santa Barbara.”