Data source: U.S. Energy Information Administration, Short Term Energy Outlook (Table 4a and Table 10b), May 2025 and Enverus Note: L48=U.S. Lower 48 states

Onshore crude oil production in the U.S. Lower 48 states (L48) has more than tripled since January 2010, driven by tight oil production growth in the Permian region. Onshore crude oil production is made up of both legacy oil production, primarily from vertically drilled wells, and newer tight oil production, primarily from horizontally drilled wells.

Legacy production decreased from 2.6 million barrels per day (b/d) in 2010 to 2.1 million b/d in 2024. Over the same period, tight oil production increased from 0.8 million b/d to 8.9 million b/d, accounting for 81% of total onshore L48 oil production in 2024. The Permian accounted for 65% of all tight oil production growth and 51% of L48 oil production in 2024.

Since 2010, U.S. tight oil production within and outside of the Permian has generally grown. Tight oil production from non-Permian plays decreased from 2015 to 2017 in a period of low oil prices. At the beginning of 2020, tight oil production from the Permian region was essentially equal to tight oil production from all other producing regions in the United States. Permian and non-Permian oil production both fell significantly in response to crude oil prices falling below $50 per barrel (b) related to the COVID-19 pandemic, with production reaching annual lows in May 2020. After 2020, however, production in the Permian increased at a faster rate than production outside the Permian.

Data source: U.S. Energy Information Administration, Short Term Energy Outlook (Table 10b), May 2025 and Enverus Note: WTI=West Texas Intermediate

Tight oil production in the Permian began growing again in 2021 as crude oil prices rose, but production in the non-Permian remained low. After 2020, Permian tight oil production grew at a slower rate than 2017–19, but by December 2024, Permian production reached 5.6 million b/d, up 45% compared with 2020. In contrast, non-Permian tight oil production decreased by 14.9% (0.6 million b/d) based on the annual average oil volumes from 2020 to 2024.

Within the Permian region, the Wolfcamp, Bone Spring, and Spraberry plays produce most of the tight oil, accounting for 99% of Permian tight oil production in 2024. The Wolfcamp play, the largest of the three, has driven growth in the Permian and produced 3.4 million b/d of tight oil in 2024, which was equivalent to production from all other non-Permian tight oil plays combined. The Spraberry and Bone Spring combined produced an average 2.1 million b/d in 2024.

Data source: U.S. Energy Information Administration, Short Term Energy Outlook (Table 10b), May 2025 and Enverus

From 2000 through 2024 the cumulative production from the Permian Basin totaled been 14 billion barrels of crude oil and nearly 40 trillion cubic feet of natural gas. In 2024, the basin accounted for about 2 billion barrels of oil and nearly 7 trillion cubic feet of natural gas production.

Permian Basin oil & gas production and gas/oil ratio (GOR) (2000-2024)

Cue Forrest Gump…

Well… Maybe not…

Let’s look at the Wolfcamp Formation

At 3.4 million barrels per day, The Wolfcamp Formation of the Permian Basin is, by far, the largest single contributor to US oil production.

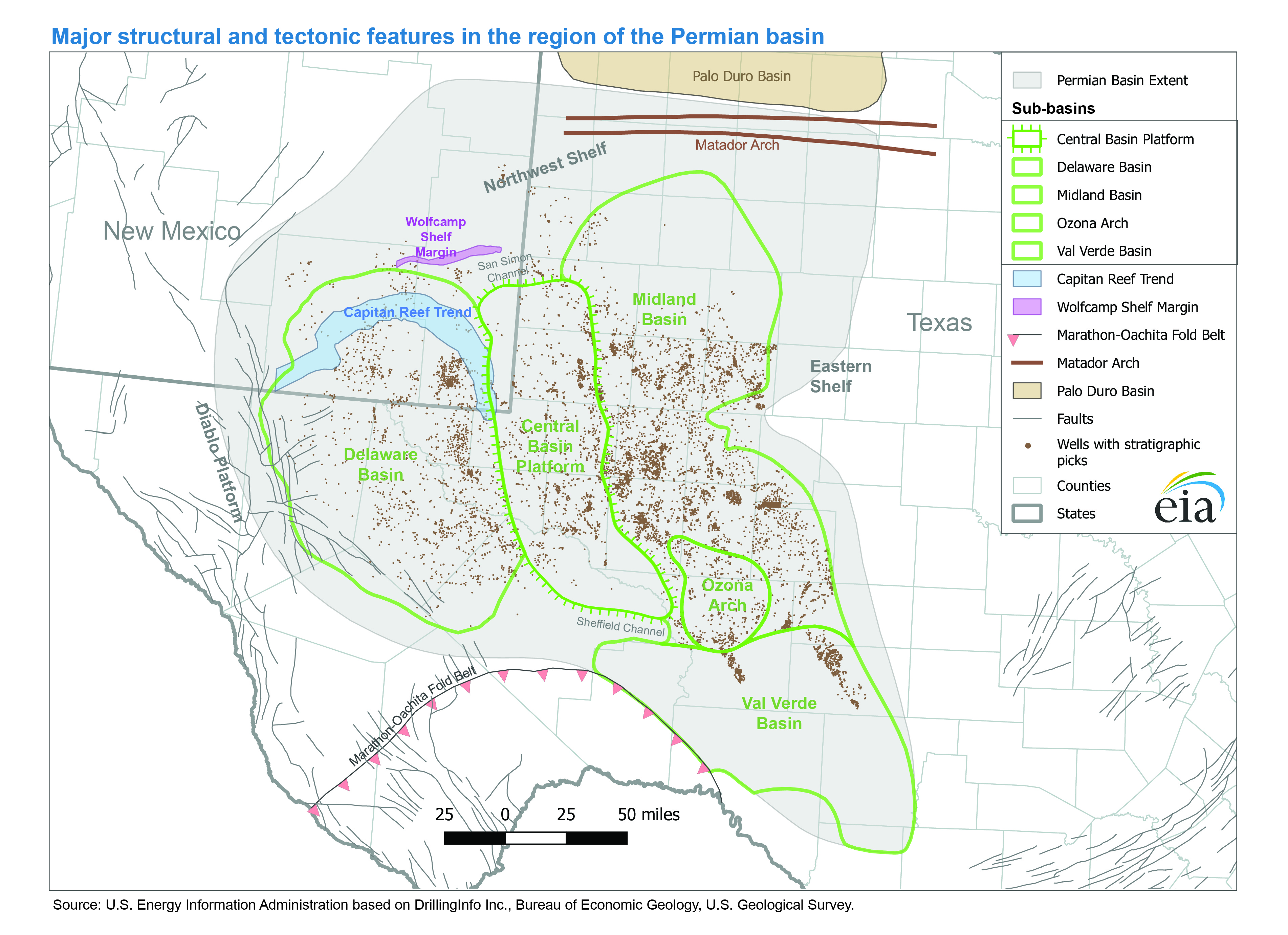

The Wolfcamp Formation was first identified in outcrops in the Wolf Camp Hills, south of the Glass Mountains, north of Marathon, Texas over 100 years ago.

This year marks a centennial celebration for petroleum geologists in more ways than one. A few months after the founding of AAPG in early 1917, the first description of the Wolfcamp Formation was published in the University of Texas Bulletin No. 1753 titled “Notes on the Geology of the Glass Mountains” by J. A. Udden, on Sept. 20, 1917.

Johan August Udden described a series of outcrops in the Wolf Camp Hills that lie at the southern end of the Glass Mountains, approximately 12 miles northeast of the town of Marathon in Brewster County, Texas.

The organic-rich “shale” was deposited in an semi-enclosed “epicontinental” sea approximately 290 million years ago.

Regional stratigraphy and lithology of the Wolfcamp formation Wolfcamp formation deposited during late Pennsylvanian through late Wolfcampian time is distributed across the entire Permian Basin. The Wolfcamp formation is a complex unit consisting mostly of organic-rich shale and argillaceous carbonates intervals near the basin edges. Depth, thickness, and lithology vary significantly across the basin extent. Depositional and diagenetic processes control this formation heterogeneity. Stratigraphically, the Wolfcamp is a stacked play with four intervals, designated topdown as the A, B, C, and D benches (Gaswirth, 2017). Porosity of the Wolfcamp Formation varies between 2.0% and 12.0% and averages 6.0%; however, average permeability is as low as 10 millidarcies3, which requires multistage hydraulic fracturing.

Throughout most of the history of the Permian Basin, the organic-rich Wolfcamp was considered one of the primary source rocks for conventional oil & gas reservoirs in the basin. The Wolfcamp was not thought to be a viable reservoir rock due to its low permeability.

The advent of horizontal drilling, coupled with multistage hydraulic fracking since 2010, rapidly led to the Wolf camp becoming the dominant oil reservoir in the United States. In 2016, the USGS estimated a technically recoverable resource of “20 billion barrels of oil, 16 trillion cubic feet of associated natural gas, and 1.6 billion barrels of natural gas liquids” in the Midland Basin alone. Since the USGS assessment, the Permian Basin has yielded 11.6 billion barrels of oil and 33.9 trillion cubic feet of natural gas, with the lion’ share coming from the Wolfcamp… And production is still on the rise.

The Austin Chalk and Tokio and Eutaw Formations of the Gulf Coast Basin contain a mean of 6.9 billion barrels of oil and 41.5 trillion cubic feet of natural gas according to a new assessment by the U.S. Geological Survey.

The USGS has completed an oil and gas estimate for the Bakken and Three Forks Formations in the Williston Basin of Montana and North Dakota. The estimate includes 4.3 billion barrels of unconventional oil and 4.9 trillion cubic feet of unconventional natural gas in the two formations. This assessment updates the 2013 USGS assessment of the Williston Basin.

The Eagle Ford Group of Texas contains estimated means of 8.5 billion barrels of oil, 66 trillion cubic feet of natural gas, and 1.9 billion barrels of natural gas liquids, according to a new assessment by the U.S. Geological Survey. This estimate consists of undiscovered, technically recoverable resources in continuous accumulations.

The Mississippian Lime (ML), a carbonate formation that primarily produces oil, underlies a large portion of Northern Oklahoma and Southern Kansas. The formation has been drilled vertically since the 1940s, with its first horizontal well drilled in 2007. The play lies at a fairly shallow depth (4,000-7,000 feet), and it features different drilling characteristics from shale and tight sands formations. Carbonate plays tend to be more permeable, which reduces the amount of drilling horsepower required to navigate through the rock. This, along with its shallower depth, tends to reduce drilling costs, everything else being equal.

The Niobrara-DJ Basin is a crude oil and liquids rich gas play that is located in Northeast Colorado and Southeast Wyoming. The Niobrara is located in several areas of the Rocky Mountains, including the Powder River in Wyoming and in parts of Northwest Colorado. The portion that lies within the Denver-Julesburg (DJ) Basin is a combination shale/marl/chalk/sandstone formation that lies at depths 5,500′-8,500′, and is comprised of three separate zones, or “benches:” the A, B, and C benches. Just below the C bench sits the Codell tight sands formation, which is more of an emerging natural gas play, but is also garnering the interest of operators, especially those who are able to drill commingled Niobrara and Codell wells.

The Cana-Woodford (also known as the Anadarko-Woodford) is a liquids rich shale formation that is named after Canadian County, OK, although the formation underlies several counties in the western half of the state. Production in the Cana-Woodford kicked off in the 1930s from conventional vertical wells, with the industry’s first horizontal well coming in 2007. More recently, however, the counties that comprise the Cana fairway have been targeted for emerging oil plays, such as the SCOOP and STACK formations.

The Cana is a relatively deep formation, ranging from 8,000′-16,000′ in true vertical depth, with some wells reaching total measured depth greater than 20,000′. In 2011, the U.S. Energy Administration went so far as to declare the Cana-Woodford the deepest commercial horizontal shale play in the world. Similar to the Eagle Ford and the Ohio-Utica formations, the Cana features a dry gas, a condensate, and an oil window.

Sorry David. We’re definitely on the back half. Novi Labs does this for a living.

“”We’ve never been in a position before where we were on the back-half of the inventory story of the Permian basin,” Novi Labs head of research Brandon Myers said.”

Yes, laterals are getting longer. But dlat length/dEUR is dropping fast. Costs are skyrocketing. Service availability is dropping, as it becomes a $ trading business, at best. Even Sec. DOE, Chris Wright’s old outfit, Liberty Energy is transitioning out of oilfield service and into portable power supply. Frac crew count is only steady because the leftover servicers have dropped rates by enough to slowly catch up on the Trumpian YUGE DUC inventory.

Candidate quality is also dropping, as infilling progresses, along with the offset interference and frac hitting that we petroleum engineers have yet to find an economic solution for. GOR’s and WOR’s are relentlessly increasing. And the low 2024 oil price will result in higher SEC abandonment rates.

All told, when the SEC 2024, proved, on permian oil reserves (the only kind that really matter) are finally added up, they will be lower, YOY. 2025, with it’s oil price certain to be about the lowest this century, and all other drags even more firmly entrenched, will continue the immutable Hubbertian, trend.

And FYI, “Drill Baby Drill”, has done and will do, next to nada to arrest the trend. Environmental, safety and health compliance costs will drop slightly, producers will continue to be allowed to shirk most insuring/lockboxing of asset retirement obligations (part of SEC reserves assessments), and those estimates will remain a fraction of actual costs for plugging miles long flat, hydraulically incompetent, laterals. But those $ savings will go for M&A, buybacks, dividends, and not for efficient drilling and completion CapEx.

Forgot to mention that much of the current production maintenance is from initial and return to production of wells shut in for oil price. Producers – understandably – got tired of waiting and went for cash flow that would girder the next 1/4erly report. Those dreamy price hikes just over the rainbow finally got reality checked…

The first oil well in the Permian Basin was drilled in 1920. If the back-half lasts as long as the front-half then the year 2130 looms large in this story. Maybe there is a long tail. [2200?] Yes. No. Maybe.

For those that expect to be around (not me), find a copy of Julian Simon’s “The Ultimate Resource” and keep it handy.

Sorry John. Think I’ll go with the data.

The hands are simply not making it to the mouth anymore, often enough to maintain the reserves/present production ratio. I.e., the stat that is actually the name of the game….

Ah, Interesting. So peak non Permian tight oil has already happened.

I am suresomeone in the comments will explain how oil isn’t actually fossil, but is continuously being formed out of bovine excrement.

Enjoy it while it lasts…

Your point is simple-minded and ignores what has driven the ongoing increase in overall oil/ gas production.

Non-Permian production is a function of cost and regulatory restriction, not of how much oil/ gas could be extracted outside the Permian Basin. There is still plenty of oil/ gas still obtainable outside the Permian Basin (continental shelves especially) but the cost to do so and/ or the regulations preventing extraction are what has been keeping non-Permian production constant the last number of years.

So, narrowly speaking you are correct. But, your point is pointless. There’s plenty of oil/ gas to be had for many more years both inside and outside the Permian Basin. It may require new technology and/ or higher prices for oil/ gas and/ or reduced restrictions.

You are making the same mistake King Hubbert made in 1956 who claimed “peak oil” would occur around 1970.

I’d like to enjoy it while it lasts and it certainly will in my lifetime, but for some reason, some people think we shouldn’t.

Ban fossil fuel use is the mantra of leftists everywhere. I say, use it while you got it. Why shouldn’t we? Remember, people who want to lower your standard of living are not your friends.

Also, if we REALLY need a replacement for fossil fuels, what’s going to power the developments of those viable replacements?

They’ve been trying to cut off what works without a viable and reliable replacement.

Let the market decide, not the Government.

They’re forcing us to put the cart before the horse by killing the horse. Where can the cart go?

Without coal, oil and gas, there would be nothing made of metal, nothing made of plastic, no electric grid, no transport except for walking and riding on animals, no communications except shouting and smoke signals, and (if it need be said) NO WINDMILLS, SOLAR PANELS, EVs, or BATTERIES.

So WTF are their non-solutions to the imaginary “problem” going to accomplish?

The words of Rick Moranis in Spaceballs come to mind…

Organic materials deposited in geologic strata represent stored solar energy (plus CO2 from air and water).

Sane people recognize them as God’s/Earth’s gifts to mankind, just like the host of other geologic materials that are useful/essential to daily life.

Thanks DM for another reminder

John Hultquist

June 4, 2025 6:53 am

TIP:

Cargo ship “Morning Midas” transporting thousands of vehicles is adrift 300 miles southwest of Alaska’s Adak Island. The Midas carries 3,000 cars, including around 800 electric vehicles. “Smoke was initially seen emanating from a deck carrying electric vehicles,” a spokesman said.

“Tight” refers to the permeability of the reservoir rock.

tight oil

1. n. [Geology]

Oil found in relatively impermeablereservoir rock. Production of tight oil comes from very low permeability rock that must be stimulated using hydraulic fracturing to create sufficient permeability to allow the mature oil and/or natural gas liquids to flow at economic rates.

David…. refresh my memory for me please… what permeability numbers are we looking at in the Permian Tight Oil formations? Thanks, from a former mudlogger

I know you’re generally Gulf of America/Texas, but do you have any thoughts on where we might be if the cretins in New York ever allowed development of the Marcellus (gas, not oil).

The extreme cynic in me says that the government of NY doesn’t give a sh** about the environment. They’re just using that as an excuse to ban exploration and development because they don’t want a huge influx of money to the central, conservative part of the state that could be used to challenge the liberal/progressive order.

The Utica likely contains more natgas than the Marcellus, and is also more extensive in New York State. It is much less developed (except in Ohio) because underlies the Marcellus (by about 2000 feet in NY and about 5000 feet in PA).

You’re right and I agree, but I think most people with just a passing knowledge recognize the Marcellus name and I think it’s what one hears about the most. Either one, or both, would be fine with me. If allowed to explore and develop, mineral rights owners would benefit from the development of both formations (I think, I’m not an exploration geologist or petroleum engineer).

ResourceGuy

June 4, 2025 11:23 am

Just so you know, having very good infrastructure and contractor base in place for production, movement, maintenance, and expansion is important for explaining oil field development rates. It takes a contractor village as Hillary would say.

Christopher Chantrill

June 4, 2025 3:57 pm

Experts agree that we are reaching Peak Permian. Activists insist that anyone that disagrees is a Permian Denier.

Australian Permian Basins (better known for coal mines) and older have plenty of oil and gas exploration and exploitation potential within the tight formations, but the anti-fracking sentiment in Australia is very strong, aided and abetted by the anti-fossil fuel mob.

Chuck Dandy

June 4, 2025 8:47 pm

I keep seeing reports indicating that he break even point for Permian oil is $65 \ barrel and a reduction of rigs from the Baker Hughs reports.

The indication is that OPEC+ wants it piece so they are keeping the price below the Permian cost. Might be tough to drive development of tight oil in Texas.

Just for the record. There is no such thing as shale oil. A molecule of oil cannot come out of a shale matrix rock in less than geologic time, unless the shale has natural fractures that are filled with oil over a few million years. The Eagleford & Bakken make oil by using poor hydraulic fracturing techniques that fracture out of the shales into oil reservoirs that have been produced vertically for decades and then call it shale oil that it is not. All horizontal plays in the Permian are in normal reservoir rock formations that have been produced in vertical wells for decades. There is shale gas, but again this is not darcy flow it is a similar desorption that has been seen in coal seams prior to the shale gas plays.

{kind=link}

{kind=link}

Old rocks! Most of the wells I logged overseas produced from formations dating from after the Cretaceous.

I’ve worked the Gulf of America since 1988… Mostly Miocene, Pliocene and Pleistocene… Not even really rocks in much of the Pleistocene section… 😉

Sorry David. We’re definitely on the back half. Novi Labs does this for a living.

“”We’ve never been in a position before where we were on the back-half of the inventory story of the Permian basin,” Novi Labs head of research Brandon Myers said.”

https://www.reuters.com/markets/commodities/us-oil-producers-face-new-challenges-top-oilfield-flags-2025-03-27/

Yes, laterals are getting longer. But dlat length/dEUR is dropping fast. Costs are skyrocketing. Service availability is dropping, as it becomes a $ trading business, at best. Even Sec. DOE, Chris Wright’s old outfit, Liberty Energy is transitioning out of oilfield service and into portable power supply. Frac crew count is only steady because the leftover servicers have dropped rates by enough to slowly catch up on the Trumpian YUGE DUC inventory.

Candidate quality is also dropping, as infilling progresses, along with the offset interference and frac hitting that we petroleum engineers have yet to find an economic solution for. GOR’s and WOR’s are relentlessly increasing. And the low 2024 oil price will result in higher SEC abandonment rates.

All told, when the SEC 2024, proved, on permian oil reserves (the only kind that really matter) are finally added up, they will be lower, YOY. 2025, with it’s oil price certain to be about the lowest this century, and all other drags even more firmly entrenched, will continue the immutable Hubbertian, trend.

And FYI, “Drill Baby Drill”, has done and will do, next to nada to arrest the trend. Environmental, safety and health compliance costs will drop slightly, producers will continue to be allowed to shirk most insuring/lockboxing of asset retirement obligations (part of SEC reserves assessments), and those estimates will remain a fraction of actual costs for plugging miles long flat, hydraulically incompetent, laterals. But those $ savings will go for M&A, buybacks, dividends, and not for efficient drilling and completion CapEx.

Dream on….

Forgot to mention that much of the current production maintenance is from initial and return to production of wells shut in for oil price. Producers – understandably – got tired of waiting and went for cash flow that would girder the next 1/4erly report. Those dreamy price hikes just over the rainbow finally got reality checked…

The first oil well in the Permian Basin was drilled in 1920. If the back-half lasts as long as the front-half then the year 2130 looms large in this story. Maybe there is a long tail. [2200?] Yes. No. Maybe.

For those that expect to be around (not me), find a copy of Julian Simon’s “The Ultimate Resource” and keep it handy.

Sorry John. Think I’ll go with the data.

The hands are simply not making it to the mouth anymore, often enough to maintain the reserves/present production ratio. I.e., the stat that is actually the name of the game….

I think your Chinese EV car is on fire in the Pacific…

It’s deja vu all over again.

A ship loaded with 3,000 cars, I read.

But only 800 were EV’s.

They wanted to be sure.

The energy is going out of the Permian, with Howard County leading the way:

Ah, Interesting. So peak non Permian tight oil has already happened.

I am sure someone in the comments will explain how oil isn’t actually fossil, but is continuously being formed out of bovine excrement.

Enjoy it while it lasts…

Your point is simple-minded and ignores what has driven the ongoing increase in overall oil/ gas production.

Non-Permian production is a function of cost and regulatory restriction, not of how much oil/ gas could be extracted outside the Permian Basin. There is still plenty of oil/ gas still obtainable outside the Permian Basin (continental shelves especially) but the cost to do so and/ or the regulations preventing extraction are what has been keeping non-Permian production constant the last number of years.

So, narrowly speaking you are correct. But, your point is pointless. There’s plenty of oil/ gas to be had for many more years both inside and outside the Permian Basin. It may require new technology and/ or higher prices for oil/ gas and/ or reduced restrictions.

You are making the same mistake King Hubbert made in 1956 who claimed “peak oil” would occur around 1970.

True… But the Permian Basin is truly a “Super Basin”…

https://wiki.aapg.org/Super_basins

I’d like to enjoy it while it lasts and it certainly will in my lifetime, but for some reason, some people think we shouldn’t.

Ban fossil fuel use is the mantra of leftists everywhere. I say, use it while you got it. Why shouldn’t we? Remember, people who want to lower your standard of living are not your friends.

If fossil fuels are banned, what fuel do you use for firetrucks and water bombers and for space heating in winter? Do these leftists have any brains?

Also, if we REALLY need a replacement for fossil fuels, what’s going to power the developments of those viable replacements?

They’ve been trying to cut off what works without a viable and reliable replacement.

Let the market decide, not the Government.

They’re forcing us to put the cart before the horse by killing the horse. Where can the cart go?

Unobtainium. 😉

No they don’t (short answer).

Without coal, oil and gas, there would be nothing made of metal, nothing made of plastic, no electric grid, no transport except for walking and riding on animals, no communications except shouting and smoke signals, and (if it need be said) NO WINDMILLS, SOLAR PANELS, EVs, or BATTERIES.

So WTF are their non-solutions to the imaginary “problem” going to accomplish?

The words of Rick Moranis in Spaceballs come to mind…

“Absolutely nothing.”

Is that a serious question, H.P.?

Organic materials deposited in geologic strata represent stored solar energy (plus CO2 from air and water).

Sane people recognize them as God’s/Earth’s gifts to mankind, just like the host of other geologic materials that are useful/essential to daily life.

Thanks DM for another reminder

TIP:

Cargo ship “Morning Midas” transporting thousands of vehicles is adrift 300 miles southwest of Alaska’s Adak Island. The Midas carries 3,000 cars, including around 800 electric vehicles. “Smoke was initially seen emanating from a deck carrying electric vehicles,” a spokesman said.

Joining the Felicity Ace and the Freemantle Highway …

Perhaps the EV business will be snuffed out by the cost of insuring these EV carriers and their cargoes,

It’s been abandoned, crew has been rescued.

https://www.carscoops.com/2025/06/car-carrier-fire-evs-abandoned-pacific-ship/

THAT Gold is devaluating Fast!

What is “tight oil production”?

“Tight” refers to the permeability of the reservoir rock.

https://glossary.slb.com/terms/t/tight_oil

Thanks.

David…. refresh my memory for me please… what permeability numbers are we looking at in the Permian Tight Oil formations? Thanks, from a former mudlogger

10 tiny Darcies?

Very tiny… a Darcy is big. Rocks with Darcy (1,000 millidarcies often require sand control measures.

Those numbers are in the article.

I’m getting very aroused by this discussion…

I know you’re generally Gulf of America/Texas, but do you have any thoughts on where we might be if the cretins in New York ever allowed development of the Marcellus (gas, not oil).

The Heritage Foundation has some thoughts on this subject…

https://www.heritage.org/energy/report/hydraulic-fracturing-and-economic-outcomes-study-marcellus-shale-counties#:~:text=Using%20the%20Pennsylvania%20data%20to,if%20the%20state's%20moratorium%20were

Thanks for the reference.

The extreme cynic in me says that the government of NY doesn’t give a sh** about the environment. They’re just using that as an excuse to ban exploration and development because they don’t want a huge influx of money to the central, conservative part of the state that could be used to challenge the liberal/progressive order.

Sounds like an accurate appraisal.

The Utica likely contains more natgas than the Marcellus, and is also more extensive in New York State. It is much less developed (except in Ohio) because underlies the Marcellus (by about 2000 feet in NY and about 5000 feet in PA).

You’re right and I agree, but I think most people with just a passing knowledge recognize the Marcellus name and I think it’s what one hears about the most. Either one, or both, would be fine with me. If allowed to explore and develop, mineral rights owners would benefit from the development of both formations (I think, I’m not an exploration geologist or petroleum engineer).

Just so you know, having very good infrastructure and contractor base in place for production, movement, maintenance, and expansion is important for explaining oil field development rates. It takes a contractor village as Hillary would say.

Experts agree that we are reaching Peak Permian. Activists insist that anyone that disagrees is a Permian Denier.

Australian Permian Basins (better known for coal mines) and older have plenty of oil and gas exploration and exploitation potential within the tight formations, but the anti-fracking sentiment in Australia is very strong, aided and abetted by the anti-fossil fuel mob.

I keep seeing reports indicating that he break even point for Permian oil is $65 \ barrel and a reduction of rigs from the Baker Hughs reports.

The indication is that OPEC+ wants it piece so they are keeping the price below the Permian cost. Might be tough to drive development of tight oil in Texas.

It’s $61-65/bbl.

https://www.eia.gov/todayinenergy/detail.php?id=65024

And OPEC+ definitely wants to maintain their market share… Maintaining a price of $60-70/bbl allows almost every player to “tread water.”

https://www.oilandgas360.com/breakeven-crude-oil-prices-are-one-metric-of-the-economic-constraints-facing-opec-members/

So… IF! Countries (USA)? were to become fiscally responsible, we would be enjoying VERY low oil prices???

Is that too simplistic?

Just for the record. There is no such thing as shale oil. A molecule of oil cannot come out of a shale matrix rock in less than geologic time, unless the shale has natural fractures that are filled with oil over a few million years. The Eagleford & Bakken make oil by using poor hydraulic fracturing techniques that fracture out of the shales into oil reservoirs that have been produced vertically for decades and then call it shale oil that it is not. All horizontal plays in the Permian are in normal reservoir rock formations that have been produced in vertical wells for decades. There is shale gas, but again this is not darcy flow it is a similar desorption that has been seen in coal seams prior to the shale gas plays.