Guest “Can you say bass-ackwards?” by David Middleton

Increased U.S. natural gas exports = higher U.S. prices: Who knew?

By Kurt Cobb, originally published by Resource Insights

February 6, 2022Few people noticed when energy reporters wrote in early January that the United States had become the world’s largest exporter of liquefied natural gas (LNG). Now, a group of U.S. senators has noticed and say those exports may be driving up heating and electricity costs for their constituents. In a letter to the secretary of energy, they are asking the secretary “to conduct a review of LNG exports and their impact on domestic prices and the public interest, and develop a plan to ensure natural gas remains affordable for American households.”

Who knew that exporting natural gas from American gas fields would raise natural gas prices at home? Well, the natural gas industry certainly knew. In the last decade, the industry was smarting under persistent low prices as it continually overproduced gas into a flooded domestic market.

It pushed for and succeeded in relaxing rules for exports in general and for expedited approvals of new export cargoes and facilities. The U.S. Department of Energy still has de facto control over most natural gas exports. But policy in the last five years has been to assist and encourage expansion of those exports.

The industry has always contended that there would be plenty of gas to go around because of the extraordinary growth in gas production from deep shale deposits that new technology can now extract. The so-called shale gas revolution, which arrived in the early part of the last decade, foretold an era of plentiful and cheap supplies—so much supply, in fact, that America would become a major exporter.

But the revolution seems to have stalled as marketed U.S. natural gas production has hit a plateau around 3 trillion cubic feet per month since late 2018.

[…]

Resilience

There is nothing resilient about Mr. Cobb’s pile of utter horst schist.

But the revolution seems to have stalled as marketed U.S. natural gas production has hit a plateau around 3 trillion cubic feet per month since late 2018.

Mr. Cobb links to the following chart to support his “plateau” platitude:

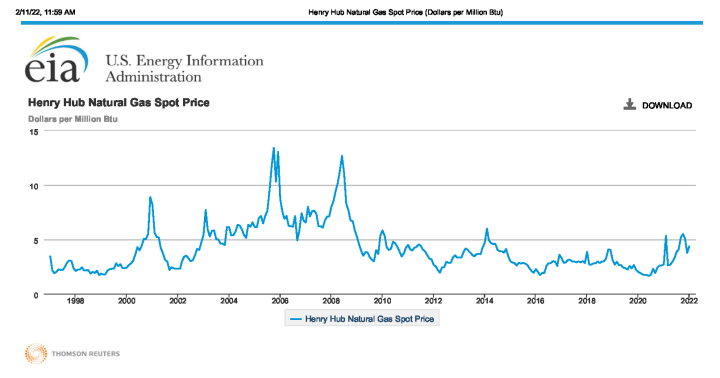

Natural gas prices have been depressed since 2014, falling below $2/mmBTU for much of 2020.

Natural gas consumption crashed in 2020, due to the shamdemic. This led to a sharp drop in natural gas production. As the economy was liberated from the shamdemic, demand for natural gas rapidly increased. Prices and production then rebounded quite resiliently. The daily production rate has already exceeded the 2019 record.

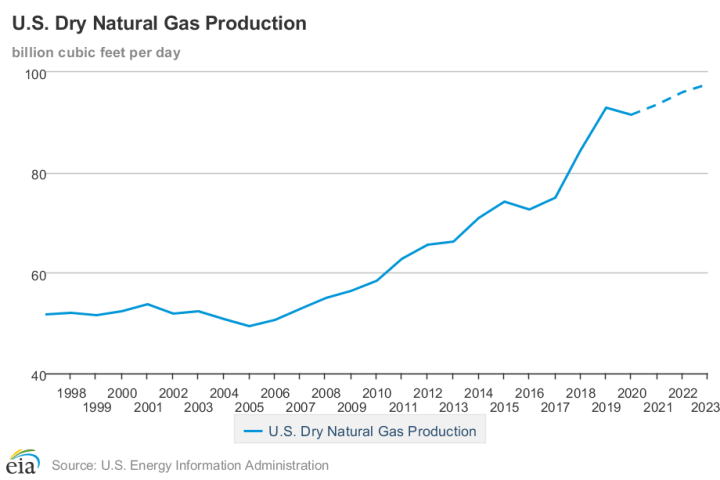

And is forecast to continue rising through 2023, supported by relatively higher natural gas prices.

U.S. marketed natural gas production forecast to rise in 2022 and 2023

In the February 2022 Short-Term Energy Outlook (STEO), we forecast that U.S. natural gas marketed production will increase to average a record-high of 106.6 billion cubic feet per day (Bcf/d) in 2023. We estimate that the natural gas spot price at the U.S. benchmark Henry Hub will average $3.92 per million British thermal units (MMBtu) in 2022, an eight-year high, and will average $3.60/MMBtu throughout 2023.

We expect that the Henry Hub price through 2023 will spur continued increases in U.S. drilling activity and natural gas production. In the February STEO, we forecast that U.S. marketed natural gas production will increase to 104.4 Bcf/d in 2022, up 2.9 Bcf/d from 2021. In 2022 and 2023, the combined marketed production from Alaska and the Federal Offshore Gulf of Mexico (GOM) will average 2.9 Bcf/d, while the remainder, around 97% of the production, will come from the U.S. Lower 48 states (L48) excluding GOM.

[…]

Natural Gas Weekly Update, February 10, 2022

The current relatively high natural gas price environment should lead to more investment in natural gas drilling & production and maintain high production rates for at least the next couple of years.

There is no shortage of natural gas, at least not in the U.S.

“Increased U.S. natural gas exports = higher U.S. prices: Who knew?“

No one knew.

At least no one who knows anything about natural gas or economics in general “knew” that increased natural gas exports equaled higher U.S. prices.

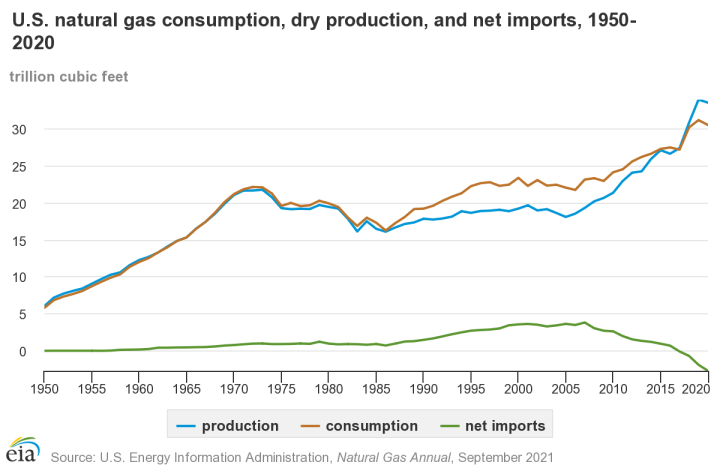

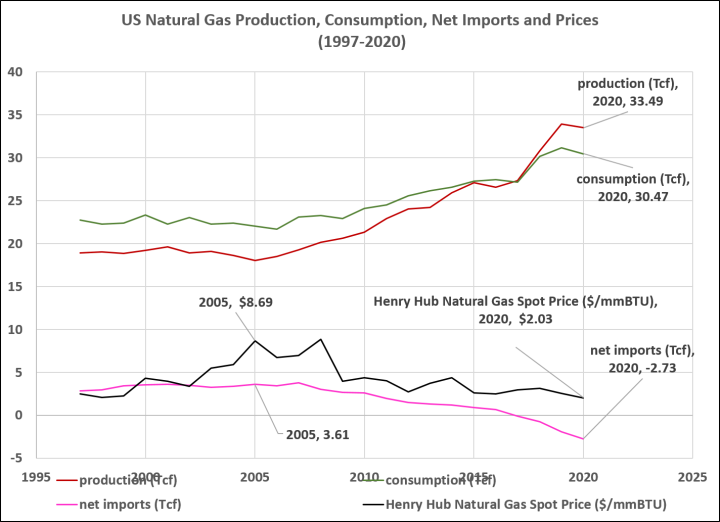

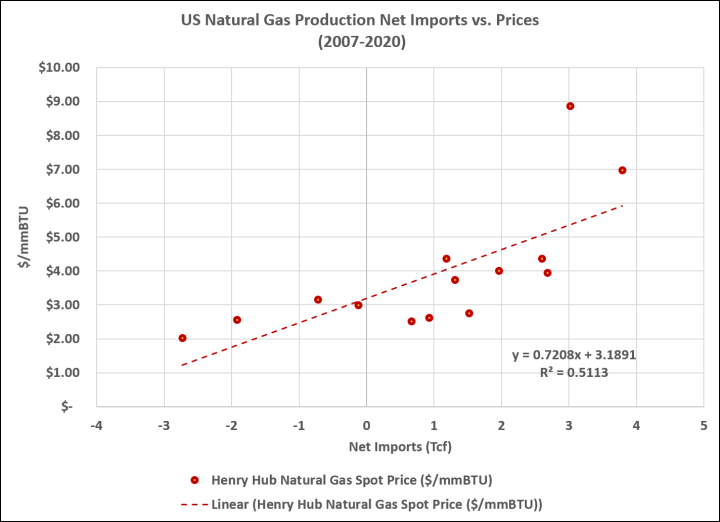

We are able to export natural gas because we produce more than we consume. If natural gas exports were prohibited, we wouldn’t have excess natural gas production.

When the U.S. consumed more natural gas than it produced, we were a net importer and prices were higher.

https://www.eia.gov/energyexplained/natural-gas/imports-and-exports.php

The relationships between production, consumption, net imports and prices aren’t particularly difficult to comprehend. While many other variables come into play, natural gas prices have had a negative correlation with the volume of gas we export since 2007, our peak year of natural gas imports.

https://www.eia.gov/energyexplained/natural-gas/imports-and-exports.php

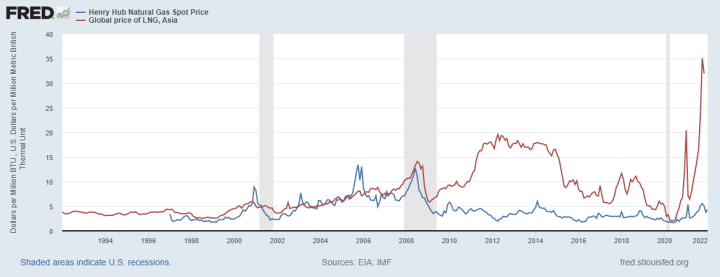

When nations produce less natural gas than they consume (net importers) they tend to pay more for the gas. Liquified natural gas (LNG) is far more expensive than domestic natural gas (Henry Hub).

https://fred.stlouisfed.org/series/MHHNGSP#0

The price in Europe for imported Russian pipeline gas is currently about the same as LNG. Europe imports most of their natural gas and pays about 10 times as much per mmBTU as the world’s leading natural gas exporter.

The moral to the story is: Increased U.S. natural gas exports imports = higher U.S. prices!

Good lesson. Good teacher. Thanks.

And as far as I know, the imports are due to Northeastern states blocking pipelines, as well as former Governor Andrew Cuomo’s jihad against fracking.

Massachusetts imports its gas from Russia!- while right next door to NY state and its 11 million acres of untapped shale gas

Well, look at it this way, Joseph: when the Massachusettians can’t get more imported gas from outside their perimeter, they can simply frack themselves to get it on their own turf. 🙂

Have a nice weekend.

no gas in Mass but there is a little coal in the Boston Basin

Jones Act, which regulates shipping between U.S. ports, has also made it prohibitively costly to ship gas from the Gulf Coast to Massachusetts.

Shouldn’t that read “… consumed more natural gas than it produced…”?

Fixed.

It is just me or does Homer look a bit like Brandon? 😎

Walter the puppet, one of Jeff Dunham’s entourage. See a Walter Press Conference:

https://www.themix.net/2021/06/comedian-jeff-dunhams-version-of-a-biden-press-conference-is-too-close-to-reality/

It would be a lot harder to tell the difference if Homer had an ice cream cone in his hand.

Technology advances match or exceed the difficulty increase in finding and retrieving the next tranche of oil and natural gas reserves. This is a good thing.

On the other hand, regardless of what you might think, oil and gas reserves are a finite resource. They are also a critical strategic resource. They really cannot be replaced with anything at this time.

The path that we should be taking is to produce just enough to keep world wide prices low, not so much that it ends up as critical strategic resources in our enemies hands. Make our enemies produce at a high rate and low price and keep our reserves available for future generations.

I do not see wind, solar, batteries or that mythical fusion energy coming along to replace these resources. Nor does it seem we will be building terawatts of clean nuclear energy either. Any thorium power plants in the wild yet?

So, my position is keep as much of ours in the ground as we can while keeping prices low and importing as much cheap stuff from other places as possible. What this means is that when prices are low we have a mechanism to slow our own production and buy from other producers and any excess is deposited for future use, and when prices become high we open the slowed taps and release the deposits to keep things as close to our favor as possible.

I have carefully studied (in parts of two published ebooks, the oil and gas resource/reserve situations both for the US and globally. There is a lot of misinformation out there, illustrated by essays Matryoshka Reserves and Reserve Reservations in Blowing Smoke.

Oil becomes a concern about 2023-25. Not a ‘peak oil’ cliff event because reservoir depletion does NOT follow Hubbert’s postulated logistics curve; it is almost always a long tailed gamma function. I illustrated using Proudhon and North Sea. Fracked oil resource doen’t help much as recovery factors average 1.5% and might reach 3%.

Nat Gas in US is NOT a foreseeable concern. Lots of gas shale, for example the almost untapped Utica underlying the Marcellus. And recovery factors are over 15% and are projected to reach 25% with more perf and prop.

So the path forward for US, IMO, is CCGT for next 40-50 years, during which time we fully develop and test a few Gen 4 nuclear concepts, of which molten salt thorium is but one. Essay Going Nuclear in ebook Blowing Smoke enumerates a number of them, as well as some obvious non-starters. Go Gen 4 nuclear when the concepts are proven by pilots and present CCGT is reaching end of life.

Rud, That would be fine if we had informed voters that weren’t insisting the government do “Something” to save the planet from the non-existing climate crisis that is not caused by burning fossil fuels.

Political reality indicates we either spend a few $trillion more on sunshine, breezes, and batteries, in the next 20 years, and wreck our economy; or we spend a $trillion or so on the nuclear technology we’ll have available this decade: NuScale & TerraPower.

You are probably (sigh) right. As an attempted fix, I wrote the books and priced them cheap to attempt to get ‘real’ info out there. Did my part. And will continue to try to do so here.

Dennis:

Sadly, it’s more than “a few $trillion”. McKinsey’s October 2021 report on costs of “Net-Zero” by 2050is in the $9 Trillion per year range.

And this report assumes 1) we will cut CO2 emissions by 50% by 2030,

2) all countries participate, and 3) the plan is executed very well.

[ I think none of those are realistic: not the economics, the politics, not even the underlying science of the purported “climate crisis”.]

https://www.scribd.com/document/555773648/McKinsey-The-Net-Zero-Transition-What-It-Would-Cost-What-It-Could-Bring-250122

If we need to extend the long term availability of oil and/or gas we should use coal in clean modern coal plants for electricity production and large industrial process heat. Those applications allow for the investment in the scrubbing technology to eliminate pollution while still being economically sound. Gas is a superior fuel for on site heating and small industry while oil is best used in transportation. Eventually coal can be replaced by nuclear for electricity. I’m not worried about what fuel will be best in 200-300 years any more than my ancestors worried about running out wood, tallow or whale oil.

Absolutely. Clean coal would buy us several centuries of energy security. Sadly, Brandon signaled that the security of energy supplies is of no concern to him when he shut down the pipeline from Canada. A near boundless supply of energy available from an adjacent, friendly nation? What possible value would that provide?

I’m looking out the 75 and 150 year range. Not the next decade or 2. That is why I would prefer to burn down their resources rather than ours. Regardless if there is more oil and gas to be found, it invariably will be harder to find and harder to recover. The difficulty will not change if we look for it and drill for it next year or 50 years from now, but our capability will be increased.

What you would “prefer” has absolutely no relationship with reality.

Natural gas is the ultimate “renewable” source of energy. It is produced by anaerobic decomposition of biologicals. It has been produced and used in sewage treatment plants and landfills for years. Nature is producing it all the time. We may develop technologies to convert coal seams to natural gas and possibly capture deep sea methane hydrates. It is clean burning in that it burns four hydrogen atoms for each carbon atom. So frack on.

fred, i did not know that NG is be produced continuously in nature. i find this fascinating and want to learn more. can you direct me to an information source that describes this process? thanks, joe

Markets will always come and bite you.

Silver Thursday.

The porter in MacBeth and “A farmer, who had hoarded his crops to sell at inflated prices during the next famine and then hanged himself when the famine never came.”

There’s still a lot of flint left at Grimes Graves, technology moved on, although in Boris’ Net Zero Britain there might be a revival in the Flint Knapping trade

“On the other hand, regardless of what you might think, oil and gas reserves are a finite resource. They are also a critical strategic resource. They really cannot be replaced with anything at this time.”

History shows that we can produce from coal everything we get from oil and gas. It’s expensive, inefficient and challenging but it can be done as Germany showed in WWll. S. Africa went down this route during the apartheid era and still use it to produce kerosene for aviation. Today China has quite a few coal-to-liquids and coal-to-gas projects.

WTF? WTI for March delivery is at $93 per barrel! I’m thinking of converting to a Black Gold geologist.

RL, likely to stay in that ballpark or a bit higher for quite a while. Two things are happening:

The average GOM deepwater breakeven price is around $36/bbl.

https://www.offshore-technology.com/comment/post-fid-deepwater-projects-gulf-of-mexico/#:~:text=Even%20as%20costs%20of%20facility,economics%20of%20deepwater%20projects%20challenging.

Although we can’t actually make FID decisions based on the daily or even monthly price fluctuations. Even if we could, the lag time between FID and first production is at least a couple of years.

Short term price fluctuations are more relevant to “brownfield” operations… step-outs, deeper pool wells and other things that can be drilled from existing platforms or close tie-backs.

In terms of exploration wells, the lag time is even longer. >$90/bbl is great for cash flow, but doesn’t affect GOM timelines much. We have to make long term decisions based on the existing price decks. WTI futures are back in the $60’s by mid-2025.

https://www.cmegroup.com/markets/energy/crude-oil/light-sweet-crude.quotes.html

On the other hand, in places like the Permian Basin, the reaction time is much quicker, particularly in the case of DUC wells. In resource plays, it’s more a matter of well spacing than “sweet spots.”

Let me see… The price in 1974 (when the market was at least somewhat unshackled) was $12.52. If that had just followed inflation, it would be $70.80 today.

A bit more than 31% REAL price increase in 48 years – not that great.

David, how serious a threat do you believe the “activist” members on Big Oil boards pose? I fear they are constraining necessary investments in the near term, and that near term oil and gas shortages will be exaggerated by Big Oil’s needless forays into greenwashing distractions.

They’re serious threats to their respective companies. They’re no threat at all to Saudi Aramco and other NOC’s. The greater threat comes from the financial institutions.

However, I think the combination of high oil & gas prices, coupled with our industry demonstrating that we are capable of employing CCS on a massive scale, will literally cut the legs out of every argument they have against oil & gas.

Let’s just expand the oilsands

It’s right there, no exploration worries, no dry holes, no risk

We know the cost, tech improves everyday, and we have the perfect use for hydrogen ( nice sweet synthetic oil).

And there is lots.

A few years ago for an energy essay in Blowing Smoke, I did a back of the envelope calculation based on fracked gas well decline curves that said a HH price of something between $3.50 and $4 (varies by shale play) would long term be necessary to keep US nat gas abundance flowing, as new wells have to be drilled each year to offset the rapid decline curves of producing wells. That is about where we are at, in part thanks to LNG exports. A good thing long term for the fracking industry, IMO.

There’s the good ole law of supply and demand …which always works … except supply responds to anticipated demand … except when it can’t …

It’s like nobody beats the stock market in the long term. Anything that involves people is hard to predict. Of course you can almost always explain it in the light of 20-20 hindsight. 🙂

There are always exceptions like Warren Buffet. And after so many decades, he isn’t just lucky like here today, gone tomorrow hedge funds.

Looked at through the right lens, Buffett is a pretty simple guy. link Anyway, he’s not a gambler.

The other secret sauce seems to the avoidance of doing dumb things. His right hand man, Charlie Munger, has a lot to say about that. link

If you devise a way to avoid the government (re: dumb things), I’m all ears.

Supply and demand works … until Government intrudes and puts its thumb on the scale.

Artificially raising the cost of the “Supplied” item and/or lowering the cost of an alternative item via subsidies.

(Of course, regulations are another tool of Government to get what it wants. ie Supply free crack pipes to combat Covid … somehow …. Psaki? …)

Don’t know what’s going on but the central Texas coast importation of windmills seems to have stopped.This is based on the Harbor Island, part of the Corpus Christi port, site where their supply for the first time in years is down to about a half dozen with no ships off loading, no signs of trucks leaving with blades or other parts. Port seems to have changed. One oil tanker out of Corpus seen leaving loaded yesterday. There is also a gas storage facility on the channel.

Where is word salad BigOil Bob to tell David that he has no idea and that we should build more windmills and solar energy panels?

The improvement of natural gas drilling productivity in Appalachia is nothing short of mind-boggling:

https://www.eia.gov/petroleum/drilling/pdf/appalachia.pdf

Storage additions last fall set a weekly record NOTWITHSTANDING the fact that back then there were a mere 105 rigs drilling for gas (that compares to a rig count of close to 2,000 back in 2008 when gas was priced at around $14/Mcf.

https://www.eia.gov/naturalgas/storage/dashboard/commentary/20211013

Corrected link to Appalachian natural gas drilling productivity report:

https://www.eia.gov/petroleum/drilling/pdf/appalachia.pdf

Typical anti energy response from the liberals. Exports increase cost for American consumers. What about wheat, want to reduce exports? it causes increased bread prices. Their playbook is manufacture nothing to reduce energy consumption and emissions and import everything to enable waving made in China climate virtue signalling flags. Any wonder why we have a trade imbalance?

And heightened sensitivity to a supply chain disaster.

People don’t seem to realize that Leftist goal is to bankrupt the fossil fuel industry by 2030 and replace it with wind, solar and battery storage…

Of course this is insane economic and societal suicide, but since when have Leftists been known for their mental stability?

Leftists’ major forms of attack to accomplish this insane goal are:

1) Severely restrict: oil leases, drilling permits, pipelines permits, new refinery permits, etc.

2) Set impossible pollution standards for the fossil fuel industry.

3) Cut off all bank services to fossil fuel companies through ESG scoring.

4) Cut off bank services to individuals, companies and institutions who either own stock and/or directly or indirectly provide services to the fossil fuel industry through ESG scoring..

5) Get anti-fossil fuel BOD appointees selected to fossil fuel companies through ESG threats.

6) Continue to push CAGW propaganda to scare the public and generate anti-fossil industry sentiment.

On a positive note, 20 states are already in the process of passing legislation which will prohibit any banks or financial institutions from doing business in their states if they use ESG scoring to allocate banking services to companies, institutions or individuals…

Leftists have gone completely insane…

Midterm and general elections can’t come soon enough…

Marijuana makes you stupid.

Road dog-san:

Attack my arguments, not me personally; argumentum ad hominem is a logical fallacy…

My comment was not directed at you. Were you not discussing “leftists?”

roaddog-san:

I’m sorry for my misunderstanding.

A sphincter says what?

7) Encourage leftwing environmental terrorist organizations to sue regulatory agencies, then settle with them by unlawfully cancelling drilling leases & permits.

David-san:

Yes, the Left demonizes fossil fuels (the literal motive force behind any advanced economy) and impossibly tries to replace them with wind, solar and unicorn farts…

The economic repercussions of this Leftist insanity will be catastrophic…

“Sue and settle” is entirely the result of activist leftwing Democrat judges baselessly declaring that Enviromarxist terrorist organizations have standing to file lawsuits on behalf of the air, water, environment, climate and the Earth.

You must be wrong, I recall Griff saying price has nothing to do with supply

And he’s always right.

Even for griff that is exceptionally stupid.

The Climate Caterwaulers, in collaberation with Big Green have created this perfect shitstorm involving NG, basically with the idiocy of shutting down coal power, and replacing it with “renewables”, but also by demanding a switch from ICE vehicles to EVs, putting even further strain on an already-weakened grid. It is madness. Then, they turn around and try to blame NG, which is simply responding to the demand worldwide that they themselves created.

Dave,

I agree with your assertion that natural gas production has lowered US NG prices, but it isn’t invalid to say that being able to sell LNG to Asia or Europe at far higher spot prices contributes an upward effect on domestic pricing. If European or Asian prices are 3x to 10x higher than HH spot prices; even with the ~1/3 operational cost impact of LNG, it would be more profitable to sell to Asia or Europe vs. Americans.

The real question then is if natural gas production is going to be consistently high enough to support both LNG exports and domestic demand – which is a different issue. And even then, as you certainly know, there are all manner of infrastructure impacts as well: pipelines (or lack thereof), etc etc.

You cannot sell more than the export capacity. Once that market is filled (assuming it is paying a premium) your next best buyer is the domestic market. They don’t have to pay export market price. If the domestic market won’t pay enough, the alternative for the producer is to shut in.

If potential production is greater than domestic demand, but less than export capacity then producers can either accept the price on exports, which will be lower than the domestic price, or shut in the export volume.

The basic formula:

Demand growth exceeding supply growth —> prices rise.

Higher natural gas prices –> More investment in drilling & production.

More investment in drilling & production –> More natural gas production.

More natural gas production —> Supply growth exceeding demand growth.

Supply growth exceeding demand growth —> Lower prices.

Lower prices —> Less investment in drilling & production.

Less investment in drilling & production —> Less natural gas production.

Less natural gas production —> Demand growth exceeding supply growth.

Lather, rinse repeat.

The ability to export LNG to Europe and Asia & pipeline gas to Mexico & Canada enables the industry to maintain excess production. It has the effect of smoothing out the highs and lows of the basic formula.

The problem is that there is a time lag between each of those steps.

It seems to me that you are assuming there will never be a situation where domestic demand is ignored in favor of higher priced LNG exports. Is this valid?

The entire point of the post was that U.S. LNG exports do not contribute to an upward effect on domestic pricing.

Not a direct link between price and shipping. Could it be that the world is expected – and acting – to decrease supply (due to near universal policies based on anti-fossil prejudice) and more demand for our supply pressures a price increase everywhere? The key price determinant isn’t export or import, but overall supply and demand.

Yes, it’s good when we are producing and exporting more. But the author leaves the door open to arguing without basis that all we have to do is export more to lower the price. Wrong linkage suggested.