With all due respect to Ozzy Osbourne, a guy that lived the rockstar life; who drank enough alcohol to float an aircraft carrier; who took enough drugs to stun a small nation; who survived all that, raised a family, survived to age 76/counting, and is worth $200 million…that’s not a madman. That’s genius. Well played, sir.

The story of natural gas markets and producers, on the other hand, can righteously lay claim to the title.

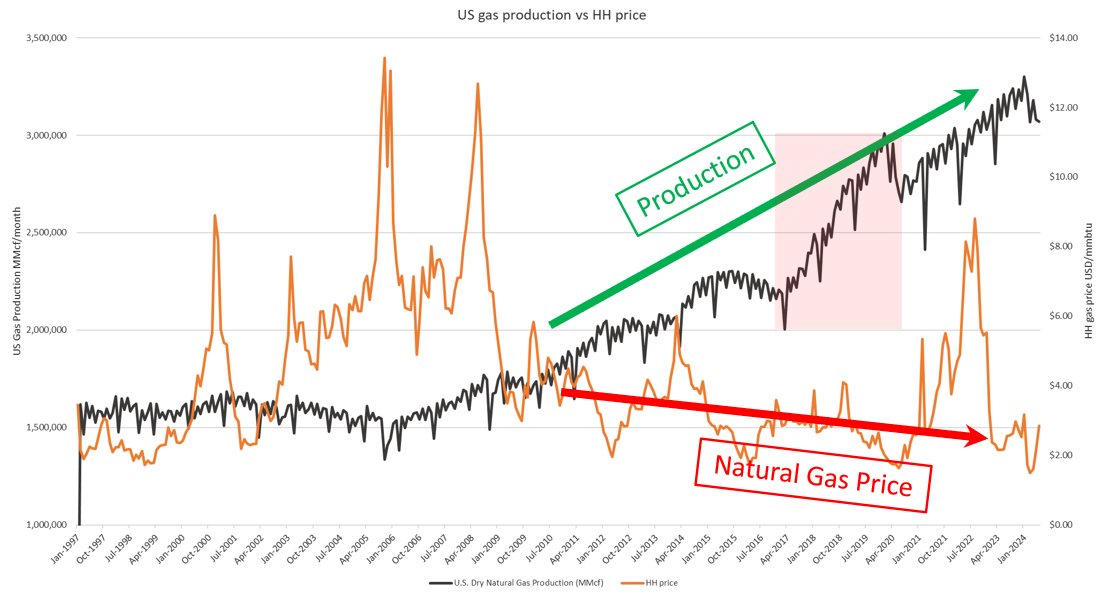

Don’t take my word for it. Have a look at this chart that depicts US natural gas production (black line) and Henry Hub prices (orange) for the last quarter century or so:

In what industry, you might wonder, would producers accelerate production at such a rapid clip, while simultaneously driving prices into the toilet. You would not be crazy in asking that. Over the period of the arrows above, the industry gave a whole new meaning to the term “value destruction”. Investors did not care for the strategy much at all, surprise surprise.

The two arrows, in isolation, do make the market look crazier than 8th Avenue at 7 pm (Calgary’s up and coming East Hastings proxy), and it is pretty bad, but, to be fair to the beleaguered participants, there is a bit of context that needs explaining.

First, the gradual increase in production from about 2006 onwards was the result of the high prices of 2002-2006, which spurred development and led to the unlocking of the US’ vast shale gas resource. High prices footed the bill for shale exploration and experimentation, which set the stage for future growth.

One of the biggest reasons for these wild trajectories is that the industry just keeps getting better and better at getting gas out of tough formations. (While there are many ways drilling and completions are improving, these advancements should not be confused with the simple act of drilling longer horizontals which is often viewed as an efficiency gain – it is a capital efficiency gain, no doubt, but not like an improved frac is – a longer lateral simply chews up the reservoir faster. One day in a decade or two we will look back and go, oh yeah, maybe that was significant…).

Those technological/fracking improvements drove the first waves of growth, but don’t completely explain the steepest part of the curve. Note in particular the pinkish shaded box, corresponding to roughly April 2017 to April 2021. Over that four-year period, the US added about 27 bcf/d, which is about 1.5 times Canada’s entire output, while prices fell from about $3.00/mmbtu to $2.00. That’s the sort of antics a guy like Warren Buffett really frowns on.

It’s true, those trajectories do look like the product of madness, but as with pretty much everything that has ever happened in history, we have to go back to the context of the times. In that period, an enormous amount of new natural gas pipeline infrastructure came into service, projects that had been kicked off some years before, in the 2014-15 timeframe, when it became clear that there was a market for all the new gas. Pipeline and gas plant builders needed volume commitments from producers to build the infrastructure, so once completed, producers did what they were obligated to do – fill up the pipe.

From a macro perspective, that kind of worked – the pipes did indeed fill up, but on the other hand the enthusiasm led to some pretty spectacular bankruptcies (hello, Chesapeake). Producers burned through vast piles of cash to flood a market that couldn’t handle the output.29dk2902lhttps://boereport.com/29dk2902l.html

The significance of this (over) development can hardly be overstated, in energy terms; in 2006 the US produced about 50 billion cubic feet per day (bcf/d); 18 years later it produces over 100 bcf/d. Early this century, some 20 years ago, the US was looking to construct LNG import terminals; 20 years later, the US is the world’s largest natural gas exporter. Now that truly is crazy.

Today, here in mid 2024, the future is murky. We know a few things: that the US (and Canada) are both capable of a lot more natural gas production. We know that demand is going to go up over the next half decade at a minimum, possibly by as much as 30 percent, due to new LNG export terminals and data center/AI demand.

What we don’t know is how easy it will be to build any new infrastructure to enable new volumes to get to where they need to be. We’re well used to this problem in Canada, of course, which is a basket case; it is a miracle that Coastal GasLink was built at all, and it is hard to imagine any entity having the intestinal fortitude to attempt any new greenfield interprovincial infrastructure, which is federally regulated, which means the ruling alliance would laugh you off Parliament Hill for even showing up with your briefcase.

The US is not far behind; the only significant interstate gas pipeline to go into service in the past few years has been the Mountain Valley Pipeline which was many years delayed by swarming activist attacks, and was completed at double the initial cost estimate (MVP was first proposed in 2014, and was scheduled to come onstream in 2018; it finally started flowing gas in 2024). A more realistic reading of the current US natural gas interstate pipeline system is this: In July 2020 the Atlantic Coast Pipeline, a large and critical new pipe that would have taken excess Appalachia gas to a thirsty US east coast, which was six years in planning, was shelved despite receiving a 7-2 vote of approval from the United States Supreme Court (from the project cancellation news release: “A series of legal challenges to the project’s federal and state permits has caused significant project cost increases and timing delays. These lawsuits and decisions have sought to dramatically rewrite decades of permitting and legal precedent including as implemented by presidential administrations of both political parties. As a result, recent public guidance of project cost has increased to $8 billion from the original estimate of $4.5 to $5.0 billion… This new information and litigation risk, among other continuing execution risks, make the project too uncertain to justify investing more shareholder capital.”)

To emphasize just how tough it is to actually build a new pipeline, Dominion Energy, one of the Atlantic Coast partners, took a $2.8 billion charge to earnings in cancelling the project. Think about that. A public company chose to eat a $2.8 billion loss rather than attempt to build a new, approved pipeline.

Of course, things are much more complicated than that oversimplification. Texas, for example, has no problems building pipelines within the state. A lot of gas is produced in Texas, and many LNG terminals are or will be located there too. So perhaps that aligns as a path for gas production growth. Similarly, AI data center owners are figuring out that they can build their data centers right alongside gas fields, bypassing a whole bucket of headaches – no interstate gas pipeline requirements, avoid grid transmission/distribution power charges, get the things built in months rather than years. So there’s another clear path between producers and consumers that might facilitate added production and consumption.

But it won’t be all that smooth. Big fields over time become smaller fields, and new developments may well be in other states. The inability to build gas infrastructure will haunt the economy in one way or another. Associated gas may or may not continue to flood the market, the amount of which available is as much a function of oil prices as anything else.

And then on top of this complicated business, layer in politics. One presidential candidate loathes hydrocarbons, and in past has supported a ban on fracking. The other candidate has sworn to cut energy prices in half, a promise which boggles the mind at the best of times, and causes cranial explosions if he’s including natural gas prices. He wants to cut those in half? See: chart above…not sure that is a well-thought-out proposal, not when it comes to natural gas anyway.

Add it all together and it is a market like no other, and it is mighty hard on the head. A wise colleague offered his own version of the above chart, a Rorschach-type interpretation that is probably a better fit for anyone involved in the natural gas business these days. The beast is obvious, if you play in this sandbox:

Whatever. Something will come up out of the blue to send the gas market into more spasms, and in a year gas prices will be fifty cents or twelve dollars or maybe both in one day. Don’t look behind the curtain please. We’re not well.

What the world desperately needs – energy clarity. And a few laughs. Pick up The End of Fossil Fuel Insanity, available at Amazon.ca, Indigo.ca, or Amazon.com.

Ozzy may not be the best example…

“”I tried a bit of burglary but I was no good at that.”

But there again, climate is rip off…

Yep: only two things you can rely on in this mad, mad, mad world: death and Texas.

And data loss.

Terry, how can you be confused about who to vote for, regarding the “layer in politics” issue, as you, all on your own, called attention to the “pinkish shaded box”, which is the prior Trump administration. Drill, baby, drill!

Problem is TheMouthX is a control freak in other subjects, and increasingly erratic.

US voters have a Hobson’s Choice.

Had an MD that had politics to the right of Attila the Hun ;)’

He called chasing bigger turnover busy bee syndrome, woe betide any Salesman who mentioned marginal pricing as a way to increase turnover. Cashflow and profit were King and if that meant shutting down half the factory to be able to increase prices then so be it.

The factory was very profitable !

Produce more, sell more, make more money. Let me guess. You went to college and that is why basic economics puzzles you?

Produce more, sell more, make more money. Let me guess. You went to college and that is why basic economics puzzles you?

He does mention associated gas, which explains some aspects of the market dynamics, at least the input of another variable.

Yes, certainly some of this gas is simply oil-adjacent.

I take it from the downvote that one of our readers has never seen a gas flare.

It still remains that basic economic reality is puzzling to the “highly educated”. Perhaps a class action lawsuit should be enjoined against American colleges for the massive brain damage they have willfully caused so many people.

And at such an affordable price. I encouraged my grandchildren to pursue time in the military, followed by careers in productive trades like plumbing … to no avail. Were I able to go back and start again, I would unquestionably become an electrician, welder or something of that nature.

Looks like a free market to me, so far dem efforts to stop this outbreak of prosperity have failed. Kamala knows exactly what she thinks about this.

As do we. Regardless of her current silence she is easily judged by her past Communism.

Gas is sold by the million BTUs. Oil is sold by the barrel. A barrel of oil is about 6 million BTUs. But the price of gas is less than 1/6th of a barrel of oil.In fact it has run around 1/36th of a barrel. This ratio first occurred early in this century.

Why does it occur? and why does it persist?

Oil and gas are different ‘goods’ with different end uses. Attempting to price them equivalently solely on the basis of energy content is very much analogous to pricing goods solely on the basis of how much labor goes into their production, aka the ‘ol Marxist (and current Democrat) Labor Theory of Value.

There is a technological arbitrage. It is possible to turn ng into liquid hydrocarbons. Why isn’t that being done?

What energy does it take?

There is technology out of Calgary AB to get more fuel out of the ‘bottom of the barrel’ by using natural gas to add hydrogen.

(The bottom is usually very thick. One refinery in NW WA makes asphalt out of it, but often it is sold cheap for other uses.)

A pilot plant may have been run in AB, there are ‘upgrader’ plants for heavy oil (one in Lloydminster treats the medium-heavy oil produced there). Publisher David Black planned to use the technology in a refinery in Kitimat BC, he was working on getting permits and financing, but drop in oil prices discouraged that, and his publishing empire went broke (and he is probably too old now to bother).

There is Fischer-Tropsch synthesis. Shell has a large facility in Qatar. The real value there though is not turning gas into low priced fuels but into high priced chemical feed stocks like Poly Alpha Olefins (PAOs).

But the liquid/gas cost differential is the basis for the midstream sector of the business. It goes basically something like this: A client has gas with high heavy hydrocarbon content (typically C2 through C5+) that they cannot bring to market because it does not meet pipeline tariff requirements. A Midstream company will process the gas to remove the liquids and replace the extracted liquids on a BTU basis with additional pipeline quality gas. The midstream company keeps the liquids as payment.

The client gets their gas to market, the midstream company makes money and everyone is happy.

The insanity of the Biden administration placing a hold on the export of the fossil-fuel most responsible for the remarkable reduction of CO2 emissions in North America reveals the stunning hypocrisy and anti-scientific posture of those claiming to be most concerned about greenhouse gases.

https://www.reuters.com/business/energy/federal-judge-halts-us-governments-ban-lng-permits-2024-07-01/

Which is only a reveal that it was never about Climate™ at all, it was about control, and keeping you the disloyal subjects from having access to cheap reliable energy.

Further, the Biden administration reducing its own geo-political leverage by cutting off the access of US producers to international markets further beclowns itself.

https://www.statista.com/statistics/253047/natural-gas-prices-in-selected-countries/

Funding the Russian war machine…

https://www.reuters.com/business/energy/russian-oil-gas-revenue-soars-41-first-half-data-shows-2024-07-03/

and what funds the US war machine, which is much more prolific?

Free market capitalism plus wealth redistribution (minus a hefty politician commission fee) to the military industrial complex. Hey, we didn’t earn the name the Great Satan for nothing ya know.

the government.

Ethane and propane are frequently found with the NG methane. They have a lot of value to the chemicals industry

There used predominately to make polyethylene and polypropylene

The analysis is incomplete without a demand curve. It is supply v demand that establishes market clearing price, not supply alone.

Also with out production cost. It’s a ridiculous analysis.

John:

Yes, but note Jevon’s Paradox: falling price increases the use of the product. Yet the geopolitical issues confound any classic market pricing.

And 3 other comments:

1) The Obama Administration’s EPA spent 3 yrs and >$35million desparately trying to find an environmental reason to kill fracking but was unsuccessful. The fracking guys invested despite these headwinds.

2) The Saudis in 2014-15 flooded the market in an attempt to “kill fracking”. As mentioned, they were successful in bankrupting a lot of companies, however the shale reserves didn’t go away. Companies like Exxon bought them for a great price. And as mentioned much of the NatGas is accompnaied by petroleum for wich the price remains good. NG is almost like a loss-leader.

3) As to Russia’s war finances: the quickest way to get Putin to the bargaining table would be for oil to drop well below $40/barrel. Good luck getting OPEC to agree to that.

“The other candidate has sworn to cut energy prices in half, …”

I am reminded of the CBS program with Art Linkletter, Kids Say the Darndest Things (1959-1967; yes I’m that old).

Trump and Musk also think 1,000 ppm of CO2 is dangerous, and J. D. Vance talks about “crazy cat ladies”. {He is on to something, but expresses this and related ideas in the darndest ways.}

Other politicians say outrageous things too, I just don’t pay enough attention to quote them.

“Trump and Musk also think 1,000 ppm of CO2 is dangerous” May I ask where you got that? Do you have a link to it?

there are many references here and there. Clearly something said in ignorance.

https://joannenova.com.au/2024/08/dear-elon-1000ppm-of-carbon-dioxide-is-safe-we-breath-it-every-day/

according to the USDA much higher amounts are not dangerous:

From https://www.fsis.usda.gov/sites/default/files/media_file/2020-08/Carbon-Dioxide.pdf

Carbon Dioxide

Health Hazard Information Sheet

10,000 ppm (1.0%) Typically no effects, possible drowsiness

15,000 ppm (1.5%) Mild respiratory stimulation for some people

30,000 ppm (3.0%) Moderate respiratory stimulation, increased heart rate and blood

pressure, ACGIH TLV-Short Term

40,000 ppm (4.0%) Immediately Dangerous to Life or Health (IDLH)

50,000 ppm (5.0%) Strong respiratory stimulation, dizziness, confusion, headache, shortness

of breath

80,000 ppm (8.0%) Dimmed sight, sweating, tremor, unconsciousness, and possible death

If all they were getting out of the ground it would not make sense to keep increasing production. They are getting C5+ condensates that are in short supply because of the need for heavy oil diluent to facilitate pumping. The value of the condensate radically impacts the economics.

Is any this really going to present a signficant problem in the future?

From the chart, from 2006 to 2009 the US was producing about 1.7 MMcf/month at a unit cost of about $7.00/mmbtu. The price then collapsed to about $3.00/mmbtu within a year.

But then the gas production grew steadily to about 3.1 MMcf/month over the next 15 years. And may continue on that trajectory for a number of the reasons mentioned in this article. Yet the price of gas has stayed around $2.00 to $3.00 (in 2009 dollars)/mmbtu in that same period, despite some temporary price boosts during the Covid Era.

So, twice the gas production at a relatively stable price.

No wonder the greenies are having a fit over fracking! They’re finding that their wind and solar fabrication, construction, backup and grid expansion/upgrading costs are climbing while fossil fuel costs are stable or dropping.

Thanks.

I note some instances in http://www.moralindividualism.com/monopol3.htm.

Including:

ALCOA prior to WW II, working hard to be more efficient and teach people how to use aluminum, increasing capacity in anticipation of demand

Aluminum fabrication companies developed an efficient process to make beverage cans, and facilitated recycling of aluminum.

Conagra, which built a large new fertilizer plant – that reduced prices in the marketplace.

Yet were attacked with government force.

The problem is there is no policy, there is nothing to stop entities like Cheasapeake Energy from drilling themselves into an oblivion along with rest of the industry. Especially when you are competing with socialist governments that have no restrictions of profitability or care about commodity prices, just raise cash now no matter how bad it hursts later. When the signs of global depletion arise, the prices will go up and conservation will be a priority, but it will be too late, and coal will be king again.

Western civilization runs on combustion just like it did when it started.