Guest “so what?” by David Middleton

IEA World Energy Outlook: Solar Capacity Surges Past Coal and Gas by 2040

11/14/2019 | Sonal Patel

Solar photovoltaic (PV) could surge ahead of coal and gas and become the largest source of installed power capacity in the world by 2035 if countries pursue stated policies and targets, the International Energy Agency (IEA) said in its newly released World Energy Outlook 2019 (WEO2019).

The agency’s annual publication, which it issued Nov. 13, suggests a major shift toward low-carbon sources is inevitable. If countries pursue existing and already announced policies (a WEO2019 scenario that was formerly known as the “New Policies Scenario,” and which the IEA renamed the “Stated Policies Scenario” in the new report), the share of renewable generation—not capacity—could nearly double, from 26% today to 44% to 2040, and it will surpass coal as early as 2026. Combined, solar PV and wind generation’s share could surge from 7% to 24%.

Solar’s explosive growth is a key change from the IEA’s report from last year (WEO2018), and the agency attributes its optimistic projections to policy changes around the world.

[…]

Fossil-fired generation could fare much worse in the Stated Policies scenario, falling below 50% of total generation in 2040—down from two-thirds, where it has hovered for decades. Coal’s generation share, which grew fivefold between 1970 and 2013, could decline from 38% today to 25% by 2040. “In 2018, final investment decisions of new coal plants were at their lowest level in a century,” the report notes. Without additional efforts to develop carbon capture utilization and storage (CCUS), “coal-fired power remains limited,” it adds.

However, natural gas-fired generation, which has tripled over the past 22 years, is set to surge nearly 50% by 2040, owing largely to the cheap shale gas supply. Yet, it will continue to hold about a fifth of the global generation portfolio by 2040, and its share could decline in Europe and Japan, the IEA suggests. Its role could also change to bolster a growing need for flexibility.

[…]

Power Magazine

“If ifs and buts were candy and nuts…”

If…

But…

“If ifs and buts were candy and nuts,” we’d save the planet. Fortunately, the planet doesn’t need saving. The planet doesn’t even notice us.

There is little doubt that solar PV installed capacity will continue to grow and could surpass coal and natural gas by mid-century. That said, the solar PV electricity output is unlikely to even catch coal by 2050. Coal-fired and natural gas combined cycle power plants are capable of delivering 85-90% of their name plate capacity. Solar PV generally maxes out below 30%. 2,100 GW of coal-fired power plants, operating at 50% of capacity, will deliver more electricity than 3,100 GW of solar PV, operating at 30% of capacity.

Natural gas will continue to kick @$$…

At least in these tangentially United States.

However, the vast majority of solar PV installations are for no other purpose than complying with government diktats.

In the AEO2019 Reference case, natural gas combined-cycle’s value-cost ratio is closest to 1.0 throughout the projection, indicating that its value just covers its costs. Natural gas combined-cycle units account for the largest share of new power plants (43% of the utility-scale total from 2021 through 2050). Solar PV’s value-cost ratio is slightly less than 1.0, indicating that, on average, its value does not cover its costs, but capacity is still added. In some cases, these solar PV additions may be uneconomic, but they still occur to satisfy the renewable portfolio standard (RPS) requirements in 29 states and the District of Columbia.

US EIA

Solar PV value is not projected to reach parity with natural gas until the mid-2030’s.

This is why the vast majority of new power plant installations in the US will be natural gas-fired, through at least 2050.

Of course, energy consumption isn’t limited to electricity generation.

It will remain a fossil-fueled world

The US EIA’s International Energy Outlook 2019 actually projects renewables to become the leading primary energy source by 2050…

However, the forecast does not indicate a planet saving energy transition. It indicates that the world will consume more of just about everything.

There has never been an energy transition, nor is one likely in the future. We burn more biomass for energy now than we did when we started burning coal.

Renewables won’t be replacing anything. They’ll just be piled on top.

•Use of all primary energy sources grows throughout the Reference case. Although renewable energy is the world’s fastest growing form of energy, fossil fuels to continue to meet much of the world’s energy demand.

•Driven by electricity demand growth and economic and policy drivers, worldwide renewable energy consumption increases by 3% per year between 2018 and 2050. Nuclear consumption increases by 1% per year.

•As a share of primary energy consumption, petroleum and other liquids declines from 32% in 2018 to 27% in 2050. On an absolute basis, liquids consumption increases in the industrial, commercial, and transportation sectors and declines in the residential and electric power sectors.

•Natural gas is the world’s fastest growing fossil fuel, increasing by 1.1% per year, compared with liquids’ 0.6% per year growth and coal’s 0.4% per year growth.

•Coal use is projected to decline until the 2030s as regions replace coal with natural gas and renewables in electricity generation as a result of both cost and policy drivers. In the 2040s, coal use increases as a result of increased industrial usage and rising use in electric power generation in non-OECD Asia excluding China.

US Energy Information Administration

About that Paris thingy…

However, it all boils down to one simple principle:

There is something dodgy about the time scale and the economics in the renewable dictation.

It took about 120 years to develop the modern infrastructure to very different levels in different parts of the world. It has been a somewhat exponential development, partly due to the extra capacity provided by the use of more practical and energy denser energy sources.

The totalitarian unicorn riders (the Greens) seem to anticipate that we will continue this exponential development trend the next 20 years, making it achievable to almost redo the whole infrastructure using long ago abandoned unpractical low density energy sources.

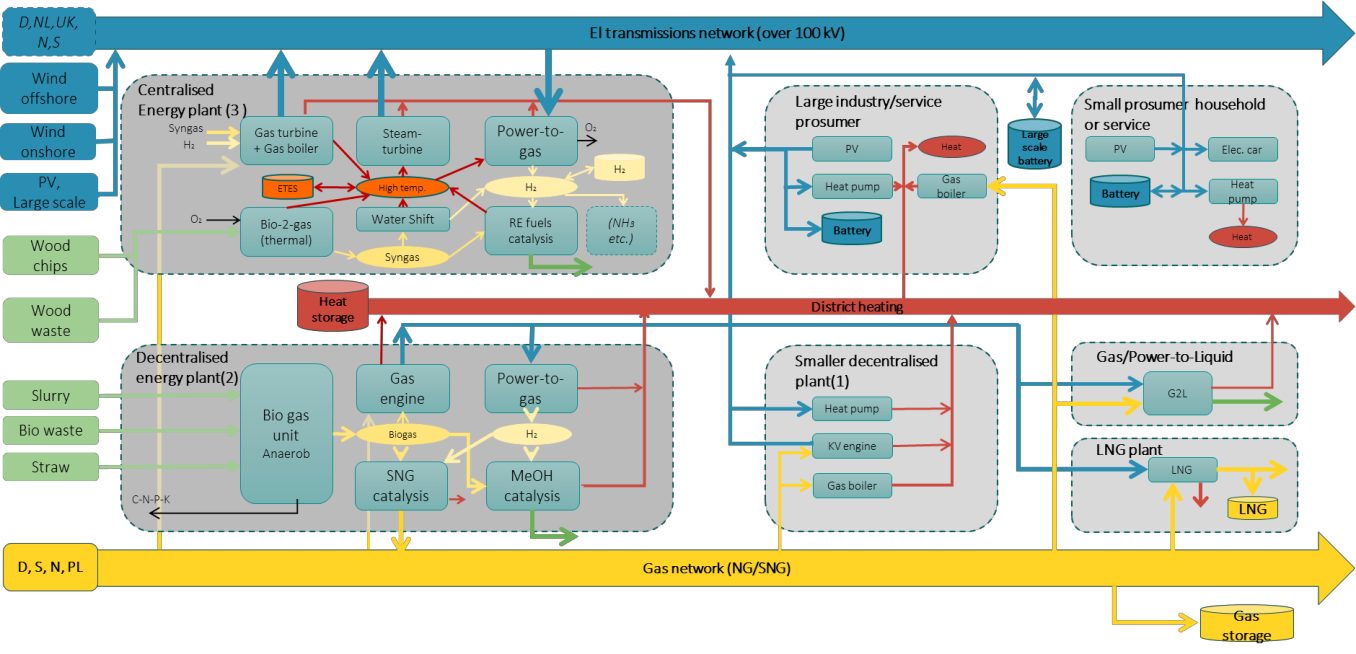

The model that is pursued is given in a report from the EU and projected to the Danish “final solution”, from where I have extracted this image:

Notice that batteries are used on virtually all scales, from grid to household. The batteries alone are bound to cost the citizens a lot in maintenance, installation, upgrade and renewals. This model is undoubtedly less costly and better achievable in northern Europe, than most other places on the planet. Have a look at the interconnections in the Baltic area with live data:

http://driftsdata.statnett.no/Web/map/snpscustom

Several countries positively help stabilize the grid, with Norway as a main player.But if Germany and Poland gets more unicorns and less conventional power, and the new gas pipeline from Norway gets build, Norway will be the determine factor, deciding price and availability of electricity and gas.

Hopefully northern Europe does not come into conflict with Norway, or it will be back to the Viking huts for the sheeple and a long walk for the elite along Bifrost to Valhalla.

My assumption is that in some regions the new IEA World Energy Outlook could go a bit along their way, but I prefer to think that their predictions from previous years are much more plausible.

The IEA must be high on something; call it Greencrack laced with Hopium. By 2040, the Climageddonist ideology will be long gone, with any remaining adherents viewed as flat-earth wackos. With the ideology supporting the “Green” faux-industry gone, wind and solar will fade from the scene as their impossibility of providing economic, reliable power becomes apparent to even once-stalwart Believers. As before the whole “climate change” nonsense started, the electric power mix of individual countries will be determined by a combination of what is most easily obtained, and politics, but certainly nuclear will see a surge, with coal and gas remaining at least as big. With the anti-coal hysteria gone, coal power will see a resurgence, taking its rightful place as a competitor to gas.

When solar panels create enough energy to build solar panels give me a call.

Thank you Seadog – I am familiar with the concept:

“And a drop of water, to release the serpents”…

Most of the time I prefer water in my Scotch, but occasionally ice is preferred to minimize dilution.

Nowadays, I drink so infrequently that it hardly matters anymore. I’ll have a glass to mark the passing of good men, or the fall of scoundrels.

Best, Allan

The magic words in such statements are always “may”, “can” or some gramatical version of these. Dont worry, will never happen.

And then along comes reality to punch them in the face.

We know what kinds of impacts the emergence of new fracking technologies have had on our ability to economically produce more oil and gas in the United States.

What about the rest of the world? For example, could China produce significantly more oil and gas than it does today by employing these new extraction technologies? What about the Middle East? Indonesia? Venezuela?

The elephant in the room that almost never gets mentioned – certainly not in the agenda-pushing liberal media – is that “power generation” (i.e. electricity) represents only about 15% of most countries’ energy use (including the US, UK). Most of the other ~85% comes from fossil fuels.

The media likes to talk about electricity generation as if it is all energy use:

“UK renewable energy capacity surpasses fossil fuels for first time”, Guardian

“The UK Now Gets More Than Half of Its Energy From Renewables”, Global Citizen

“11/14/2019 | Sonal Patel

Solar photovoltaic (PV) could surge … ” There’s the weasel word ‘could’, right in the very first line.

30% sounds a bit high, like maybe by a factor of 2. It seems like location would have a lot to do with what actual capacity factors turn out to be.

“… Solar photovoltaic (PV) could surge ahead of coal and gas and become the largest source …”

Jimmy Hoffa could regain the Presidency of the Teamsters any day now.

Elvis could be alive and frequenting Burger King. Just ask the Weekly World News.

Elvis is dead. Former Atlanta Falcons coach Jerry Glanville used to leave 2 tickets for Falcons home games at the Will Call window, just in case Elvis showed up… Until…

Either than or the steady diet of Whoppers clogged his arteries to no end.

The IEA must be using climate-models for their forecasts.

Society will be extremely wealthy in the future in order to be able to afford huge installed capacity of effecively useless energy sources.

Society will be extremely poor in the future because society wasted its wealth on huge installed capacity of effecively useless energy sources

There fixed it for you

Installed capacity and actual generation are two separate metrics. People will celebrate that we spend money to install more renewables but won’t understand that we are going to be burning more fissile fuels. I have a technical background and worked in utilities for almost four decades. I have younger relatives with political science degrees who always want to explain the science and technical aspects of future electric generation.

The holidays will again be fun this year.

John Endicott

November 22, 2019 at 8:50 am

Dennis, you’re too nice. Telling him where he can shove the apostrophe would be my preferred response to a grammar Nazi.

Upon further reflection you’re absolutely correct. Jeff really is a jerk. I’m looking forward to reviewing his future postings.

fossil fuels to continue to meet much of the world’s energy demand –> fossil fuels continue to meet much of the world’s energy demand.

In the 2040s, coal use increases as a result of increased industrial usage and rising use in electric power generation in non-OECD Asia excluding China –> In the 2040s, coal consumption increases as a result of increased industrial demands and rising consumption in electric power generation in non-OECD Asia excluding China.